Five years ago last week, the Bank of England cut its main interest rate to 0.5%, the lowest level in its 320-year history. It also embarked on its quantitative-easing (QE) programme, using printed money to buy government bonds. The aim was to inject money into household and company bank accounts, which it hoped would stimulate economic activity. In total, the bank bought £375bn worth of bonds.

In December 2008, the US Federal Reserve had already started the first of what would turn out to be three phases of QE. The Fed bought mortgage-backed securities as well as government bonds. The basic idea was that the electronically-created cash would drive up bond prices and lower yields (bond prices and yields move in opposite directions). This would (hopefully) cut borrowing costs and stimulate economic growth. The Fed has so far spent around $4 trillion of printed money on bonds.

Has it worked?

We cannot know what would have happened if QE had not been launched, as Economist.com notes. But judging by the progress of Britain and America’s economies since the crisis, it was hardly a roaring success. In Britain, GDP is 11.7% higher than it was at the worst point of the recession, but has yet to return to the pre-recession peak. The unemployment rate was 7.2% in the first quarter of 2009 – last month, it was at the same level. In the US, meanwhile, the economy has grown at a sub-par 2.4% a year since mid-2009. Payrolls are still a million jobs below their peak. So the recovery has been lacklustre by post-war standards.

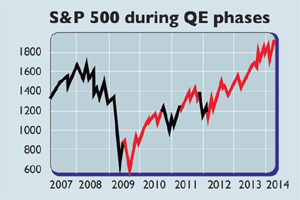

However, QE has lit a fire under stocks. Risky assets usually respond well to monetary easing. With investors expecting QE to keep going for some time, and yields on ‘safe’ government bonds being driven to rock-bottom levels (forcing investors to buy riskier assets in the hunt for yield), stocks took off. America’s S&P 500 has almost tripled since the March 2009 bottom. The FTSE 100 has soared from 3,700 to 6,800 now. Corporate bonds have also soared.

Pushing on a string

So why didn’t QE give the economy much of a boost? “The financial crisis and Great Recession changed the way consumers, bankers, business owners and managers thought and behaved,” says Gary D Halbert of Halbert Wealth Management. In effect, the crash shocked people, and made them focus on paying off debts (‘deleveraging’). When banks, households and firms are in this ‘hunkering down’ mode, simply making more money available and lowering interest rates won’t necessarily encourage them to borrow and spend. So to an extent, central banks have been ‘pushing on a string’. In Britain, too, lending has been subdued in recent years and is now expanding at just 0.2% a year. It may be several more years until the debt hangover from the bubble is fully worked off and most people and companies are ready to borrow and spend freely again.

Storing up trouble

Not only has money printing not been very effective, but it could well lead to economic and market turmoil in the future. One fear is a surge in inflation. Much of the printed cash has been hoarded by banks, so it is not moving around the economy very quickly. But as the credit freeze thaws and banks start lending again in earnest, velocity will rise rapidly, pushing inflation higher if central banks don’t act.

Another problem is that markets are increasingly detached from the fundamentals. The bigger a bubble gets, the more damage it will do when it bursts. But central banks are loath to turn off the taps and raise interest rates before the recovery looks fully secure, especially with economies still groaning under massive debt loads. Can central bankers, who never saw the crisis coming, finish QE without creating another one?