When it comes to investing, the financial world likes to see a good story for people to buy in to. Yet, often these ‘story’ stocks are the worst kind of shares to buy, as the hype never turns into reality. So there’s nothing wrong with dull, if you can make money from it.

And when it comes to dullness, the subject of polythene and plastic bags is probably near the top of the list.

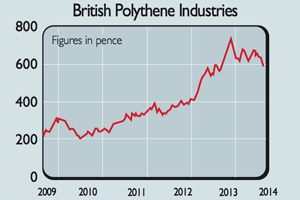

This company makes its living from manufacturing and selling these things. It strikes me as a decent business that has been ignored by lots of people because it’s just not interesting enough. I reckon it made a return on capital employed of 14.8% in 2014 – not stellar, but none too shabby either.

Like a lot of companies whose profits move up and down with the economic cycle, British Polythene Industries (LSE: BPI) has had its fair share of problems over the years.

It was hit very hard by the last recession and had to cut its dividend. Thankfully, its troubles seem to be behind it now and in recent years profits have been growing nicely and are expected to keep on doing so.

The company has been investing money in new plant and equipment to make itself more competitive. During the last few years it has also repositioned itself to focus on areas that can grow but at the same time are not too volatile.

BPI gets nearly three quarters of its sales from sectors such as agriculture (silage bags, crop protection, fertiliser and animal feed bags), food packaging, health-care and waste recycling. It gets most of its profits from mainland Europe.

BPI has been aiming to profit from the growing trend towards thinner polythene films as companies try to cut their packaging costs, and it is making good progress on this. It should also benefit from improving construction activity in the UK.

There are some risks though. The strength of the pound is becoming a big problem, as it makes exports more expensive and hits overseas profits when they are converted back into sterling. However, BPI seems to be coping so far.

The other issue is the price of its key raw material – polyethylene – which is closely linked to the price of oil.

Should we see a spike in the oil price, then BPI may find it hard to recover any extra costs from its customers. It also has a sizeable pension fund deficit that needs tackling.

City analysts are cautiously upbeat and expect another year of decent profits growth. Yet the shares trade on less than ten times projected earnings. Even with the potential risks, these look relatively cheap and could be worth tucking away.

Verdict: a risky buy