After the latest downward lurch in commodity prices, investors in the mining sector have now endured terrible returns for five years. The gold price has nearly halved and the FTSE 350 Mining index has dropped by a gruelling 75%, returning investors to where they were more than a decade ago.

There is, however, nothing better than a prolonged bear market to filter out the best fund managers. Using the industry’s dire performance as a litmus test, which funds have actually added value – the whole point of active management – in the last five years? Sadly to say, the short answer is “none”. The performance of the best-regarded mining funds available to UK investors has been unwaveringly dismal. The longer answer is “some, a little bit, but not enough to justify the fees”.

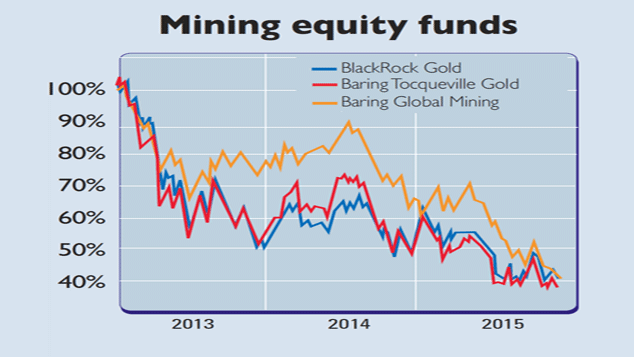

Uninspiring performance

A carefully selected actively managed equity fund should be able to outperform in down markets, cushioning investors from the mining industry’s worst volatility. To some extent, they have done that. For example, the Evy Hambro-run BlackRock Gold and General fund (which has an ongoing charges figure (OCF) of 1.92%, according to Trustnet), came to be regarded as the mining sector’s most prominent equity investor during the last bull market.

Over the last five years it has dropped by 70%, a grim performance, but still better than a 78% drop in its benchmark, the FTSE Gold Mining index. Indeed, according to Citywire it’s the top performer of seven funds in its sector. “Investors are very aware that we are going to perform in the direction of the gold price,” Hambro has told the Financial Times, “but they expect us to outperform our benchmark.”

However, the small margin of outperformance is hardly inspiring – no one is going to cheer on a 70% loss, after all – and is largely attributable to the small amount of cash (currently 2.2%) that the fund holds on the sidelines to manage its relentless flow of redemptions. Its assets under management have plunged from $3.4bn in 2011 to £681m at the end of last month, as the City has turned its back on mining investments.

Lack of conviction

With nearly 50 holdings, Hambro’s Gold and General fund is hardly high conviction in terms of its calls, particularly given the small size of the sector – but other prominent mining funds have even less conviction. The Smith & Williamson Global Gold and Resources fund (OCF – 1.82%) has 73 holdings, while the John Hathaway-run Tocqueville Gold Fund (which uses the Philadelphia Gold and Silver index as a benchmark and has a net expense ratio of 1.24%) currently has 72.

With so many companies in each portfolio, a manager’s individual stock selections are heavily diluted and it is hard to see how they can hope to add any value. So it’s not that surprising that the performance of each has been near-identical: the three funds mentioned are down 58%, 59% and 62% respectively over the last three years.

One fund with slightly higher conviction – though it also has a broader remit – is the Baring Global Mining fund, managed by former mining analyst, Clive Burstow. It holds around 30 stocks and is heavily overweight Rio Tinto versus industry leader BHP Billiton.

Burstow, however, has turned 180 degrees on Glencore in recent years and assets under management are just £5m. Its overall performance has, meanwhile, been pretty much identical to the sector’s other funds: over three years, it is down 59% and the fund’s launch in 2012, at the tail end of China’s investment boom, is proof in itself that fund managers have no special insight into the mining cycle.

Better to go passive

The regrettable conclusion is that not one mining equity fund – and these are among the best in the sector that we’ve looked at here – has been able to use the current downturn to distinguish itself from peers. Quite the opposite: mining funds appear to be huddling around their benchmarks, seeking safety in the fact that their performance will not be that much worse than peers.

The reality is that if you are currently keen to invest in gold miners (and, as Edward Chancellor argued a few weeks ago in MoneyWeek, now does look a promising time to do so), but you would rather not take the risk of researching and investing in individual companies, then you would be better off finding a cheap passive tracker to avoid paying fees on an active fund.

One such fund is the Market Vectors Gold Miners (LSE: GDX) exchange-traded fund, which tracks the biggest listed gold miners. It’s had a similarly rough time over the last five years – down around 75% – but the expense ratio is around 0.53%, meaning less of your returns will go on fees.