I have been thinking about the nightmare carry trade scenario. In other words, what is the worst possible situation for carry trade players?

For those unfamiliar with the term ‘carry trade,’ I will use the definition found on Freebuck.com.

“Carry trade – The speculation strategy that borrows an asset at one interest rate, sells the asset, then invests those funds into a different asset that generates a higher interest rate yield. Profit is acquired by the difference between the cost of the borrowed asset and the yield on the purchased asset.”

The nightmare carry trade scenario: the six conditions

I view the nightmare scenario something like the following:

1. End of quantitative easing (QE) in Japan

2. End of ZIRP in Japan (Rising interest rates)

3. Rising interest rates in Europe

4. Falling interest rates in the U.S.

5. Tightening credit in the U.S.

6. A rising yen vs. the U.S. dollar

The nightmare carry trade scenario: quantitative easing has ended

Quantitative easing has already ended in Japan. Quantitative easing simply means excessive printing of money by the Bank of Japan in order to defeat the deflation that has been raging for about 18 years.

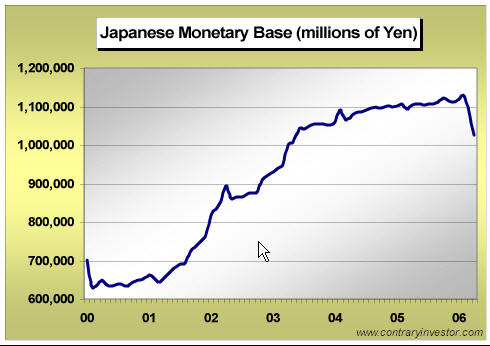

I believe that ZIRP (zero interest rate policy) and QE (quantitative easing) prolonged Japan’s deflation, but for now, that is irrelevant. The key point is that both are about to come to an end. Proof of the end of QE can be found in the following chart, courtesy of Contrary Investor:

As you can see, money supply in Japan nearly doubled between 2001-2006. Hedge funds could borrow yen at zero percent and invest in the U.S. stock market; or gold; or silver; or, after all of these rate hikes, U.S. Treasuries and get 5%. The only real worry was the yen rising in value more than the return on other investments. With Japan unwilling to let the yen rise, players piled high on the carry trade.

From a US dollar perspective, when interest rates were slashed to 1%, another possible carry trade was to borrow funds in US dollars and invest in gold, silver, or equities. With the S&P dividend ratio under 2% and interest rates close to 5%, the US carry trade slowly died with each rate hike.

Rising interest rates in Europe and Japan and falling rates in the U.S. (a global equalization of interest rates) will end more of these carry trades.

Contrary Investor points this out:

‘Historical periods of meaningful rate of change decline in the Japanese monetary base have preceded each meaningful US recession of the last three decades. Just eyeing them out, these large percentage drops occurred in ’73/’74, ’79/’80, 1990, and 2000. If, indeed, history has the chance of repeating itself ahead, what should we now be expecting for the macro US economy as we look directly at current Japanese monetary base contraction?’

Speculation in various markets is extreme, as noted by trillions of dollars worth of derivatives floating around. The unwinding of those derivatives and any related carry trades is not likely to be a smooth event.

I have previously talked about the European Central Bank running ‘stress tests’ to see if it could handle a derivative meltdown. We might just be put to the test. Clearly, we are at a serious crossroads of the greatest liquidity experiment the world has ever seen, with multiple players, in multiple countries, doing mind-boggling things with tremendous leverage.

Right now, we see the “Fed in a Quandary” about what to do. In spite of that, Bernanke thinks the Fed can magically control the global economy with a looming U.S. recession on top of a housing bubble bust. It is the height of hubris.

The nightmare carry trade scenario: Japan’s zero interest rate policy

QE is toast. Let’s consider the end of ZIRP (Zero Interest Rate Policy). Bloomberg is reporting, “Yosano Says Japan Must Eventually Say Deflation Over”:

“Japan’s government will eventually need to declare an end to deflation, Economic and Fiscal Policy Minister Kaoru Yosano said.

“‘At some point citizens will need to be told by academics or politicians that sustained price declines have ended,’ said Yosano, who was speaking to lawmakers in Tokyo today. ‘Hardly any consumers are under the impression that prices are falling.’

“Japan’s core consumer prices have risen for the past six months, signaling the economy’s tussle with more than seven years of deflation is ending. Rising prices and an expanding economy may prompt the Bank of Japan to raise borrowing costs for the first time in almost six years as soon as July, economists say.

“Chief Cabinet Secretary Shinzo Abe reiterated separately that the central bank should keep borrowing costs near zero to support the economy. He said the bank and the government need to work together to end deflation and ensure prices don’t resume falling. Abe was speaking to reporters at a regular news conference in Tokyo today.”

For now, Japan seems unwilling to let interest rates rise, as evidenced by the Financial Times article “BOJ Injects $13 Billion Into Market to Cut Rates”:

“The Bank of Japan on Monday injected a massive Y1,500 billion ($13.3 billion) into the money market as it desperately sought to keep overnight interest rates under control.

“The injection came as overnight rates once again tested the 0.1% ceiling, calling into question the central bank’s ability to keep rates at ‘effectively zero,’ in line with its stated policy.”

The market is attempting to force Japan to hike. Japan is resisting. With a national debt of 150% of GDP, how much longer can Japan resist? A rising yen would be bad for those borrowing in yen and investing in US Treasuries. A rising dollar is bad for those borrowing US dollars and buying gold, silver, or falling US dollar-denominated assets.

The crosscurrents on some of these trades are significant, even though the yen and the dollar cannot both fall relative to each other. What can happen, however, is falling asset prices (stocks, gold, silver, copper, equities) at a rate greater than any interest rate differential. That is likely in a monetary tightening situation as we are seeing in both Japan and the U.S.

The nightmare carry trade scenario: EU money supply

Writing for the Financial Sense Market Wrap Up on May 31, Paul Nolte had this interesting commentary:

“Many fingers are pointing to money supply (or lack of M3 being reported) as a key to the ‘blown-up’ US economy. However, the reality points to places outside the US. The various Ms are running at relatively low year-over-year rates – MZM 3.9%, M2 4.5%, and M1 a measly 1.8%.

‘This contrasts with the big inflation years during the ’70s and ’80s, when these aggregates were well over 10% (and sometimes north of 15%). Even the monetary base is growing at a 4% rate, less than one-third of the pace of the early ’90s. So where is the liquidity coming from?

‘One place is Europe, where the European central banks are boosting money supply by a torrid 8% annual rate. While ‘Helicopter Ben’ may have a tough name to overcome in the months ahead, investors need to look elsewhere when complaining about excessive monetary growth.”

Bingo. Once again, ‘dollar bears’ only point out what the US is doing, forgetting about gross distortions in Japan, Europe, and the UK. Long term, this is, of course, good for gold, but short term, the unwinding of various carry trades can wreck havoc on those that are overleveraged.

With that excessive expansion of credit in Europe, interest rates in the EU are poised to rise. Please be prepared to click off No. 3 on the list above if and when it happens.

The nightmare carry trade scenario: the Federal Reserve pauses

No. 4 is a given. The Fed at some point will pause. The unwinding of the housing bubble in the US assures it. The question is when. The problem if it does not pause is that the blowup of the housing bubble will accelerate, and the problem if it does is a potential bond market revolt.

Jobs here are the key. Falling jobs in conjunction with a housing bubble bust will let the Fed get away with a pause and subsequent cuts. This, of course, is where it gets complicated. Will Japan react to slowing US demand by attempting to weaken the yen yet again? If internal demand in China and Japan picks up, Japan can perhaps happily keep hiking. If not, can Japan can abruptly end QE and go back to ZIRP to fight one more round of deflation? I think not.

Everyone talks about hyperinflation in the US. What happens to the Japanese if they stay on its current QE/ZIRP path forever? At some point, a national debt at 150% of GDP matters even if ‘they owe it to themselves.’ It might seem funny to be talking about massive inflation in Japan, but under the right circumstances, I could foresee a loss of faith in the yen. Typically, emergence from K-Winter is a slow event with slowly rising inflation, but with central bankers everywhere taking all sorts of untried experiments with liquidity, some sort of major currency problem with the yen is possible.

If the BOJ changes its mind about QE (something I do not expect), then a loss of faith in the yen is certainly possible. It is a scenario that is on virtually no one’s radar, yet it is not really that far-fetched (even if at this point it is unlikely).

Yet everyone assumes the US dollar will blow up. The contrarian in me suggests that if a huge currency problem of some sort emerges, it just may be elsewhere. Perhaps this scenario unfolds sometime down the road in a panic move by Japan to reinstate QE.

The nightmare carry trade scenario: credit tightening

Let’s move on to No. 5. Is credit tightening in the US so unlikely? I think not. All it takes to kick it off is accelerating housing declines. The ultimate nightmare scenario for US housing would be a situation in which long-term mortgage rates decouple from the 10-year Treasury note and stubbornly refuse to drop in the face of easing actions by the Fed.

I view that as a possibility that I have not heard discussed elsewhere. Rising default risk could potentially change mortgage lending standards in situations in which large downpayments are not made.

Regardless of whether that specific scenario unfolds, consumer credit is showing signs of stress and money supply growth is far greater in the EU and China than it is in the US. In fact, money supply in China is up a staggering 22%.

Falling home prices, falling jobs, and a correction of the negative savings rate in the US is all that it will take for huge credit problems in the US to surface. At this point, all three of those seem extremely likely.

The nightmare carry trade scenario: a rising yen

Some have argued that with interest rates in Japan at zero, a modest rise in interest rates to 1% will not stop the yen carry trade. Borrowing at 1% in Japan get 4-5% in the US – what could be simpler?

I disagree. A rise in the yen greater than the interest rates’ differential would cause a loss for yen carry trade players. Assume for a second that rates fall to 4% in the US and rise to 1% in Japan. At that point, the U.S. Treasury yield will still be over double the dividend yield on the S&P (a situation not that great for US dollar carry trade players). And from the perspective of the yen carry trader, all it would take to wipe out profits would be a mere 3% rise in the yen.

Notice that it would not take a collapse of the US dollar to cause huge problems. A mere 6% move versus the yen would cause a tremendous amount of damage. I suppose one could try to hedge that currency risk, but ask yourself how well Fannie Mae has done hedging its interest rate risk. It may not be the easiest thing to do.

An additional problem for Japan is that a rising yen would hurt Japanese exports. That might not bode well for the Japanese stock markets. As long as Japan could slow the rise of the yen via ZIRP and QE policies, yen carry trade players had the green light to pour it on. That green light is now a brightly flashing yellow (possibly even red) given that every increase in Japanese interest rates will help fuel a rise in the yen.

There you have it: the nightmare carry trade scenario. All in all, it looks closer than anyone might have thought. Perhaps that is the message of a 100-point plunge in gold; copper going down lock limit several times; silver ramping to the moon, just to fall off a cliff; various emerging markets indexes plunging; and global equity markets taking a collective nose dive.

Should a nightmare unwinding of various carry trades unfold as I expect it to, ‘dry powder,” as cold hard cash, just may be a good thing to have.

By Mike ‘Mish’ Shedlock for Whiskey and Gunpowder.

Whiskey & Gunpowder is a free, twice-per-week, e-mail service – for more from the team, go to https://www.whiskeyandgunpowder.com.