This article is from MoneyWeek Asia, a FREE weekly email of investment ideas and news every Monday from MoneyWeek magazine, covering the world’s fastest-developing and most exciting region.

Sign up to MoneyWeek Asia here

“The time to buy is when there’s blood in the street,” is one of investing’s most famous clichés. When all is chaos, fear is widespread and investors are fleeing, it’s time to do the opposite. To the brave go the biggest returns – or so the theory goes.

But like most advice that urges you to buy at the bottom, there’s a problem. How do you know there’s enough blood on the streets? After all, in anything short of a nuclear war, things can always get worse. What looks like carnage now may look like a nosebleed just a short while later.

Thailand is a classic example of this dilemma. Its political problems have been building steadily for months. At each stage, the question rises: is it time to buy? So far the answer is “probably not yet”…

Thailand’s tangled mess

Thailand’s political problems are a tangled mess. But they come down to the ongoing struggle between associates of former prime minister Thaksin Shinawatra and a loose grouping of urban residents, royalists and businessmen, who call themselves the People’s Alliance for Democracy (PAD).

The Thaksin faction has comfortably won the last three elections with support from rural Thais. Some vote-buying and electoral fraud probably took place, but these are generally seen as the fairest elections in Thailand’s history and Thaksin won on the strength of his policies: he is genuinely popular with the rural poor for providing improved healthcare and microcredit schemes.

But the PAD refused to accept both Thaksin – who was pushed out in a military coup in 2006 – and the two Thaksin-friendly prime ministers who have held office since democratic rule was restored last year. Through a combination of increasingly violent protests – including occupying government buildings and Bangkok’s airports – and increasingly petty lawsuits, they’ve succeeded in making it impossible for the government to work.

Earlier this year, prime minister Samak Sundaravej was ludicrously forced to step down when the constitutional court found he had violated the constitution by hosting a cooking show on Thai television. Last week, the PAD won a major victory when Sundaravej’s successor Somchai Wongsawat (who is also Thaksin’s brother-in-law) and several other senior politicians were banned from politics for five years for vote-buying and three Thaksin-supporting political parties dissolved. Thaksin himself is in exile after being convicted in absentia of corruption charges, although he continues to meddle from outside the country.

The role of the king

None of the parties involved in this mess emerge looking very good. The accusations of corruption and authoritarianism levelled against Thaksin and many of his colleagues have some evidence to back them up. But the PAD are an unpleasant rabble, whose choice of name is an total misnomer – they want to replace Thailand’s elected parliament with a largely appointed one, arguing that rural voters are too ignorant to be allowed democracy.

And there’s a further elephant in the room in the shape of King Bhumibol Adulyadej, who wields enormous influence behind the scenes when he wishes to. The king dislikes Thaksin and his associates and doesn’t want them in power; it’s widely accepted that the military coup had tacit backing from the king and that he is quite happy to see the PAD’s protests succeed.

The king’s failure to support democratic governments against street protests is not helping Thailand to become more stable. What’s more, it’s clearly undermining the legal system: the courts pursue cases against Thaksin’s cronies vigorously, believing this is the king’s wishes, while granting virtual immunity to PAD members. And of course, it’s impossible to discuss the king’s role in the mess in Thailand, because the country’s draconian lèse-majesté laws mean a prison sentence for anything more critical than “long live the king”.

Investing in Thailand: cheap for a reason

So where does Thailand stand now? Well, since Somchai was forced out, the PAD has abandoned its protests – but in the short term, the damage has been done. The high-profile chaos at the airports will hammer Thailand’s vital tourism industry, while business and consumer confidence has been badly hurt by the months of uncertainty. Capital Economics expects the Thai economy to contract by 1% next year, with the risks clearly on the downside.

The long-term outlook is no better. None of the recent moves solves Thailand’s problems: the clash between the will of the rural majority and the resentment of the urban elite. Over the weekend, it appeared as if the opposition Democrat party might form a coalition with some of Thaksin’s former coalition partners, but it’s hard to see this combination being stable in the long run.

This political swamp makes Thailand a pretty unattractive investment, even though in many ways it appeals to my contrarian instincts. Another great investment cliché is Warren Buffett’s “be greedy when others are fearful” and investors are clearly very fearful when it comes to Thailand.

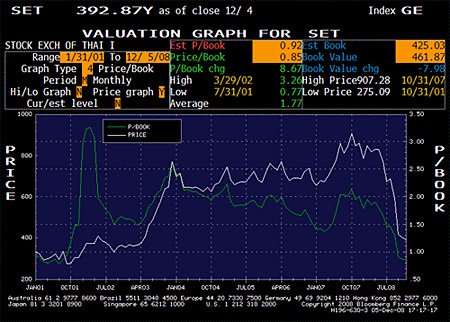

Valuations look compelling, as you can see in the chart below: the price/book ratio (the green line) is 0.85 times, which is on a par with levels in 2000-2001 when the country was still struggling with the aftermath of the Asian crisis. A dividend yield of over 8% provides a lot of leeway even if earnings fall and dividends are cut substantially.

But there’s good reason why the SET is so cheap; as we’ve seen above, Thailand’s problems are deep-rooted and not easily resolved. Unlike most of the rest of Asia, the country is clearly backsliding on governance – and given all the challenges ahead, that’s not good. While there are a few Thai stocks that look attractive, I’d prefer to avoid the broader market until the political situation quietens down – which might be a long time.

Ezra reviews its orderbook

Time for a quick update on our offshore oil services play, Ezra Holdings (SIN:5DN). A week ago, the company announced that it’s reviewing its orders for five multi-function support vessels in view of the financial crisis (i.e. it’s likely to cancel one or more of them).

Given that oil has dropped to under $42 a barrel at the time of writing, it’s no surprise that service providers are cutting back their expansion plans. Keppel, the Singapore yard where Ezra has placed its most recent order and the first to be reviewed, also announced at the same time that orders for two jack-up rigs and a semi-submersible rig for other firms are under review.

While this news tells us that the industry fears some pretty tough times ahead, I think this announcement is more positive than negative. First, any cancellations will cut the amount of debt that Ezra takes on over the next few years. Although Ezra says that funding for the MFSV at Keppel has already been secured, with credit markets volatile and the outlook for charters on new vessels less certain, reducing its debt load is prudent right now.

Second, if – as looks likely – cancellations will be widespread across the industry, this will mean a tighter market for vessels when the cycle picks up. A cutback in E&P activity and worsening decline rates at old fields mean that oil is likely to rise very sharply as soon as the global economy picks up and service providers that make it through the next couple of years in good shape will do very well.

I’m certainly not judging Ezra a buy again yet, but the firm is making the right moves in the circumstances. Although it’s still down 65% from when I tipped it, the stock has come off its September lows – and more importantly, still looks cheap on a forecast p/e of 3.8.

But oil has fallen much more than I expected and credit markets remain frozen, so the outlook is still very unclear and it’s not a time for new investors to pile in. In my view, Ezra is still a risky hold with considerable upside if all goes well.

Strong results from Vitasoy

Soy drink producer Vitasoy (HKG:0345), our China consumption stock, reported first half results last week, and the news here is much more encouraging. Sales were up 20% year-on-year, including a 60% rise in China and 22% in Australia and New Zealand, the firm’s two main growth markets. Sales in China accounted for 22% of overall sales, up from 16% a year ago. This steady rise is an important part of the investment case for Vitasoy – the firm is a solid defensive stock with a faster growth business hidden under the surface.

Profits before tax were down 2% year-on-year, but that includes a one-off provision for holiday pay for employees arising from recent court cases in Hong Kong. Excluding this, profits were up 16%. Losses at the North America business narrowed slightly and chairman Winston Lo commented that the unit is expected to return to profit in the next couple of years.

That said, Vitasoy is cautious about the outlook, saying that the remainder of the year will be “increasingly challenging” and that its sector will be affected by the global financial crisis. Management is being commendably honest – even a defensive business like Vitasoy is bound to be affected to some extent and we can’t expect anything like the same growth rate in the next set of results, even in China (I’ll take a detailed look at the latest news on the Chinese economy in next week’s email).

As you can see on the chart below, Vitasoy is down over the last few months, falling 18% since I tipped in back in September. But it’s outperforming the Hang Seng benchmark, which is down 33%, and with a stable business, good dividend and a strong financial position (large cash reserves and total borrowings to equity of just 9%), I’d expect it to continue to do so as the global economy deteriorates.

Turning to the markets…

| Market | Close | 5-day change |

| China (CSI 300) | 2,013 | +10.0% |

| Hong Kong (Hang Seng) | 13,846 | -0.3% |

| India (Sensex) | 8,965 | -1.4% |

| Indonesia (JCI) | 1,202 | -3.2% |

| Japan (Topix) | 786 | -5.8% |

| Malaysia (KLCI) | 838 | -3.2% |

| Philippines(PSEi) | 1,889 | -4.0% |

| Singapore (Straits Times) | 1,659 | -4.2% |

| South Korea (KOSPI) | 1,028 | -4.5% |

| Taiwan (Taiex) | 4,225 | -5.3% |

| Thailand (SET) | 393 | +0.8% |

| Vietnam (VN Index) | 300 | -4.8% |

| MSCI Asia | 73 | -3.6% |

| MSCI Asia ex-Japan | 253 | -3.5% |

Asian equity markets slid last week on the steady stream of bad economic news, both at home and in the West. The exception was China, which rose 10% on a combination of government plans to boost the economy and direct purchases of shares by state-controlled funds – the latest government move to prop up the market.

In the credit markets, there were signs that funding is becoming tighter even in Japan. The three-month Tokyo interbank offered rate – the rate at which banks can borrow from each other – rose to just under 0.9%, compared with the overnight target rate of 0.3%. Interest rates in the Japanese commercial paper market – short-term borrowing by companies for working capital needs – have risen even further. Yields on one-month CP for A1-rated companies stood at 1.8% on Friday; back in September they were around the same level as the interbank rate.

On Monday, there was fresh uncertainty over the direction of Chinese currency. Ahead of US Treasury Secretary Henry Paulson’s visit to Beijing for talks on economic co-operation, the renminbi slid by 0.7% against the dollar, the biggest daily fall since China began allowing the currency to float in July 2005. This prompted contracts based on its value in a year’s time to jump to 7.35RMB/USD before easing back slightly, on fears that China might devalue the renminbi in a effort to help struggling exports – a move that could risk starting a damaging international trade war – see Trade war may be brewing between China and the US.

In Hong Kong, property stocks fell after statistics showed real sales slumping to a 17-year low in November. Just HK$10.6bn in units were sold last month, down 87% year-on-year, according to Land Registry data. And in India, IT consulting and outsourcing giant Infosys closed the week down 8% after reports that it will freeze new hiring ahead of an expected slowdown in the industry. Other IT firms including Satyam, Tata Consultancy and Wipro also slid.