Falling house prices, a tightening mortgage market, banks having to be bailed out by the government, rising unemployment. Sound familiar? Welcome to Dubai.

When the credit crunch first struck, “the capital of bling looked set to buck the global downturn”, says Peter Conradi in The Sunday Times. But figures are now emerging that show the desert region’s property prices are not just falling – they are plummeting. According to Colliers International – a property consultancy firm – house prices fell by 8% in the final quarter of 2008 in Dubai. Although property prices in the region rose 59% in 2008, HSBC research found that property prices fell by 23% in the fourth quarter. And things could be about to get nastier, with UAE bank Shuaa Capital forecasting that prices will fall 60% in 2009.

Colliers International blames the rapid turnaround on speculative investors. Having bought property from developers, hoping quickly to sell it on for a profit, they are now unable to sell as the credit isn’t there for others to buy. “The music has stopped, the finance isn’t available and the developer is asking for his money,” says Ian Albert of Colliers in The Times.

Worse, this is uncharted territory for property investors and the real-estate industry in the United Arab Emirates. Dubai’s property market is very young. It was only in 2002 that foreign investors were given permission to buy property in the area. A deluge of foreign money then transformed what had been a sleepy desert village into a sprawling metropolis of new skyscrapers and reclaimed land projects. As a result the Dubai property market hadn’t experienced a downturn until recently. So no one knows quite what to expect.

The new spectres haunting Dubai – as prices fall and property developers and construction firms lay off thousands of workers – are negative equity and repossessions.

“It wasn’t that long ago when to utter Dubai and default in the same sentence would have evoked derision,” says Keith Parker, the conference manager of IIR Middle East in UAE newspaper The National. “Today, negative equity and repossessions are becoming… part of the business language.” Stricter lending practices brought in by banks as a result of their fears of rising defaults means many investors can’t get the money to pay final balances to developers and can’t sell as new buyers can’t raise funds either.

This throws up two major problems for Dubai. Firstly, it is not yet clear how the banks will cope with defaults by the many foreigners living in the state. “If I default on my mortgage and I decide to go back to Pakistan, what is HSBC going to do about it?” asks a Dubai-based banker in The Times.

The other fear is how the country’s new Mortgage Law will perform, as it remains untested. As things stand if a bank chooses to foreclose it faces a potentially long and expensive battle to recover arrears through the civil court. “Here, you can’t have your home repossessed if it’s your only home. Under the Islamic way in the UAE, a debtor won’t be put in jail or have his home taken unless it’s the very, very last resort,” says Ibrahim al Sukhi, the general manager of Credit Rating and Collection, a debt collection firm, in The National.

So the danger is that more of Dubai’s banks may follow the lead set by Amlak Finance and Tamweel, two UAE banks that were bailed out by the government last November. Meanwhile, more and more investors are being left with properties they can neither afford, nor sell.

A week in the property market

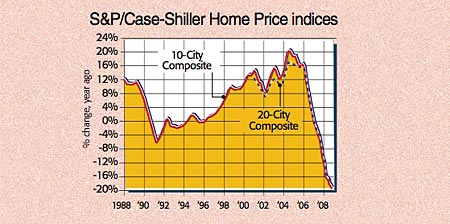

• American house prices continued to fall in November, according to new data from Standard & Poor’s. Indeed, the S&P/Case-Shiller Home Price index shows price drops for single family homes right across America. Eleven of the 20 areas showed record rates of annual decline. “The freefall in residential real estate continued through November 2008,” says David M. Blitzer, chairman of the Index Committee at Standard & Poor’s. The 10-City Composite fell 19.1% – the same record decline as in October – while the 20-City Composite fell a record-breaking 18.2%. Phoenix and Las Vegas have had the worst year, with prices down 32.9% and 31.6% respectively.

• Australia’s Gold Coast is also experiencing nosediving property prices, with one property selling this week for $5.5m less than its value six months ago. The 963 sq m beachfront property on Main Beach Parade near Surfers Paradise sold at auction for A$9m six months after the owners rejected a A$14.5m offer. The owners were described as “obviously disappointed” in The Australian.

• The number of mortgage approvals fell by 52% last year, according to the British Bankers Association (BBA). “The banks approved less than half the 2007 number of loans for house purchase, reflecting falling demand from households facing greater economic uncertainty and double-digit falls in house prices over the year, which led to a wait-and-see mentality,” says David Dooks of the BBA on BBC News.

• UK house prices suffered their biggest annual decline since 2001 this month, according to research firm Hometrack. Prices fell 9.4%, leaving the average house price at £158,300.