Finding a decent return on your money is becoming ever harder for income-hungry investors, but one promising option is investment trusts, says Alice Ross in the FT. Several of these publicly listed companies, which invest in the shares of other listed companies, have built up their cash reserves in the boom years. Unlike unit trusts, investment trusts only have to pay out 85% of the income they receive each year to shareholders, allowing them to keep the rest for leaner times.

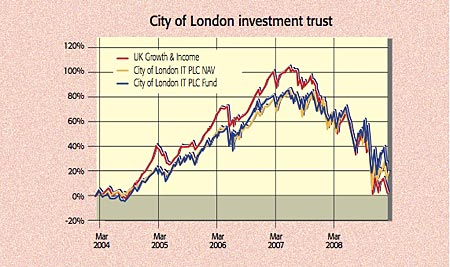

This means that even if the companies they have invested in are forced to scrap dividends to conserve cash, the trusts should be able to maintain payouts. Indeed, the City of London Investment Trust (LSE:CTY), for example, which yields 5.8%, has increased its annual dividend over each of the last 42 years, while Alliance Trust (LSE:ATST), Bankers Investment Trust (LSE:BNKR) and Caledonia Investments (LSE:CLDN) have all paid out for the last 41 years. Even with times as tough as they are now, nearly every trust in the UK Income Growth sector has dividend cover of at least a year, says The Daily Telegraph, with the average yield now more than 6%, against 4.8% on the FTSE All Share.

This good news may come as a surprise to investors, partly because many financial advisers keep quiet about investment trusts. Why? Because they receive no commission for recommending them, which is one reason why investment trusts have lower fees than unit trusts. There are other advantages. Because investment trusts are traded on the stockmarket, their share prices can suffer big short-term fluctuations. That means their market capitalisation at any given time can be above or below the value of their net assets. A big discount isn’t good if you need to sell up quickly, but it’s great if you’re a buyer – if a trust trades at a discount to net asset value (NAV) of 10%, it means you’re getting £1 worth of shares for 90p. In terms of risks, investment trusts can borrow money to invest, though not all do. This can boost returns in the good times, but can leave them vulnerable when times get tough.

The downside just now is that because investors are so keen to find reasonable sources of income, you are unlikely to find trusts trading at big discounts to NAV. So anyone buying now may find that when they come to sell, the discount has widened rather than narrowed. But if your aim is to find a decent yield, an investment trust is a cheaper bet than unit-trust equivalents, and carries less risk than buying individual stocks. City of London (see above) is a solid fund, while Neil Woodford’s Edinburgh Investment Trust (LSE:EDIN) looks another good bet, yielding 5.7% on a discount of 5.9%.