Since the start of the bear market, shares in Capita have beaten the FTSE 100 by 35% because fund managers have thought it a safe buy. But you can always pay too much for a stock, even a quality one such as Capita.

The group is Britain’s largest provider of ‘business process outsourcing’ (BPO), including call centre, administrative and IT services, split almost 50/50 across the public and private sectors. The basic idea is that customers outsource their non-core operations to Capita, who then integrate them within its larger activities, cutting costs while improving service. This is a win-win situation for both parties. As a result Capita expects its top line to keep growing at low double-digit rates – it’s already bagged £767m in new work this year, against £1.24bn for the whole of 2008. But I suspect much harder times are just round the corner.

Capita Group (LSE: CPI), tipped as a BUY by Seymour Pierce

BPO is becoming much more cut-throat, with rivals including Serco, IBM and Accenture. There are also serious risks in the sector in general. These include the dangers of delays in signing new deals; the mis-pricing of services; cost over-runs; negative press coverage (for example, Jarvis’s role in the Potters Bar rail crash); and/or the loss of a major customer. Capita is by no means immune to these – in October 2007 it lost its flagship contract to operate London’s congestion-charging scheme. It will now have to hand the project (worth around £60m a year) to IBM in November.

The same goes for its financial services unit (accounting for 29% of sales). This could soon be hit by the credit crisis as banks downsize their operations. What’s also slightly odd is that the group does not disclose the size of its order book, although it happily reports the £3.1bn bid pipeline. There may be nothing to worry about, but even so it does raise questions over transparency.

For 2009, the City is forecasting sales and adjusted earnings per share of £2.75bn and 38.56p respectively, rising to £3.0bn and 43.8p in 2010 – putting the shares on a toppy 18 times p/e ratio. I would rate Capita on a forward enterprise-value (EV)/earnings before interest, tax and amortisation (EBITA) multiple of ten. Adjusting for the £596m of net debt and the £100m pension deficit, this generates a value of 450p a share – around 35% less than current levels. I’d advise cautious investors to exit while the going is good, especially as its juicy 13% operating profit margins could come under attack from low-cost rivals. The chief executive and operations director recently offloaded 223,000 shares to bank a £1.45m profit – follow their lead.

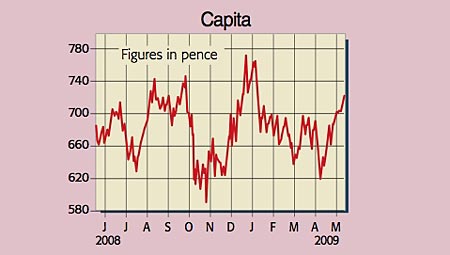

Recommendation: SELL at 710p

• Paul Hill also writes a weekly share-tipping newsletter, Precision Guided Investments