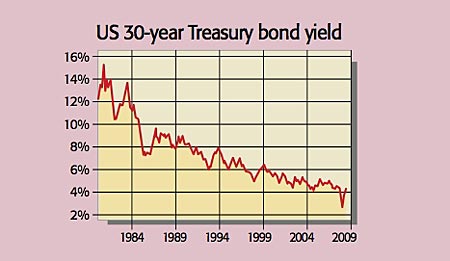

Whether March marked a true low for stocks isn’t clear, but “the asset market that has the highest probability of having made a secular high is the US long-term government bond market”, says Marc Faber in the Gloom Boom and Doom Report. Yields (which move inversely to prices) on the 30-year T-bond have rebounded to 4.32% after falling to as low as 2.52%.

Part of that rise “is due to the sheer supply of government debt scheduled for the next few years, which spooks many investors”, says Niels Jensen of Absolute Return Partners. “But countries such as Australia and Canada, which suffer only modest fiscal deficits, have experienced rising rates as well, so it cannot be the only explanation.” Most likely, the end of the “safe haven argument” for buying government debt is also playing a part.

“With the financial crisis seemingly ebbing, many investors are moving out of Treasuries into riskier and potentially better-performing areas, including high-yield bonds and stocks,” says Larry Light in the Wall Street Journal. After all, the T-bond has enjoyed a spectacular bull market since 1982, when the end of a “corrosive inflationary era” lead to strong returns for long-term bonds.

But at just 2.5%, yields weren’t giving much protection against the risk of a resurgence in inflation further down the line – and even 4.5% doesn’t provide a lot of leeway. So while the US government isn’t yet having trouble issuing debt – new bond auctions are still selling out easily, albeit with less bidders than before – it looks increasingly likely that the panicked rush into T-bonds in December may have marked the “last hurrah” for that 26-year bull market.