In an abrupt about-face, the American Commodity Futures Trading Commission (CFTC) is “considering sweeping changes to commodities trading to stamp out the excessive speculation that has been blamed for the volatility of oil prices”, said The Independent’s Stephen Foley.

Gary Gensler, the new head of the CFTC, has said his agency will look at imposing limits on the maximum size of positions held by traders in “commodities of finite supply”, especially energy commodities.

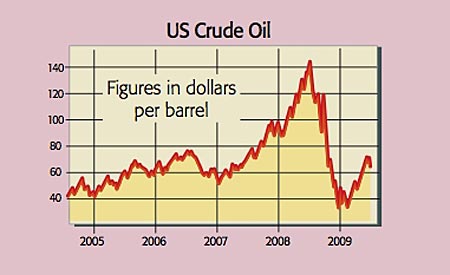

What the commentators said

That’s a big turnaround from last July, said the FT. Back then, oil prices were a lot higher, yet “a multi-agency task force led by the CFTC reported that speculators only react to prices rather than drive them”.

But much has changed in the last year: “a new president, a Democratic supermajority in the Senate and a drastic weakening of financial institutions’ political clout.” In this very different climate, curbs on speculation look likely.

The proposals aren’t universally popular. “Simplistic rules” based on the idea of “excess speculation” are likely to be harmful, said Dwight Cass of Breakingviews. After all, “one person’s speculator is another’s welcome provider of market liquidity”.

In any case, “it is rich that elements in Washington should still blame speculators for stronger oil prices”, said Liam Denning in The Wall Street Journal. “Last year’s oil spike was likely exacerbated by energy officials filling the Strategic Petroleum Reserve despite a squeeze in supply.”

No, said Nils Pratley in The Guardian. Common sense and hedge-fund managers say the amount of money flowing into long-only commodity funds played the key role in driving the price of oil to $147 a barrel last summer. “Messing about with markets is dangerous”, but so are the distortions that are caused by the weight of money flooding into these markets. “Modest restrictions on commodity trading make sense.”