Vindon is a leading UK manufacturer of niche climate chambers, and also provides associated services to the pharmaceutical, life sciences, heritage and food sectors. Vindon’s 43 on-site storage suites allow customers to deposit their drugs and clinical trials for up to, say, five years, in order thoroughly to test how the materials react under various environmental conditions, such as temperature, humidity and sunlight.

Big pharma currently represents the lion’s share of the business. Stability testing is an essential part of bringing new compounds to market and recent regulatory changes mandate that raw materials and semi-finished products also now need be tested. Vindon is also seeing good take-up of its new services, such as disaster recovery, NHS blood bank, and stem-cell storage services.

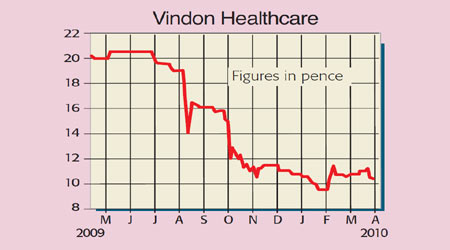

House broker WH Ireland sees 2010 sales coming in at £5.8m and earnings per share at 0.9p, rising to £6.2m and 1.1p in 2011. This puts the stock on undemanding p/e ratios of 11.4 and 9.3. Moreover, at last month’s preliminary results, the dividend was hiked 10% to 0.165p, demonstrating the board’s confidence in the firm’s prospects.

Chairman Liam Ferguson reiterated the encouraging outlook: “The fundamentals remain very strong. Our financial position and the substantial investment in the new facilities provide a sound base from which successfully to exploit our broader offering in diversified markets.” So with the wind back in its sails, and with an expected boost from America to boot, I would not be too surprised to see broker forecasts upgraded as 2010 draws to a close.

Vindon Healthcare (Aim: VDN)

What’s more, given the international angle, I believe performance could double over the next five years, delivering 2015 sales of £11m and operating profit margins of 30%. Assuming I’m right, then using a ten-times multiple, adjusting for the £2m of net debt and discounting back at 12%, the stock would be worth about 18p a share.

So what are the possible snags? Of late, sales of manufactured products have been soft as clients have put off capital expenditure. Moreover, the business is operationally geared with high fixed costs, while liquidity can be thin.

This means that if you do decide to buy, then I would recommend drip feeding any purchases into the market (up to a maximum of 13p a share), thus avoiding the risk of artificially bidding up the price.

Recommendation: BUY at 10.25p (market cap £9m)

• Paul Hill also writes a weekly share-tipping newsletter, Precision Guided Investments