A successful long-term investor needs to put recent movements in various asset classes in perspective. Enter the annual Credit Suisse Global Investment Returns Yearbook, written by Elroy Dimson, Paul Marsh and Mike Staunton of the London Business School. It spans 113 years of data across 25 countries.

The first basic message is that stocks beat bonds or cash over the long term. Global equities have returned an annual 5% after inflation since 1900, bonds 1.8% and cash 0.9%. For Britain, the figures are 5.2%, 1.5% and 0.9% respectively. British stocks have also beaten bonds since 1950 and 1980. In global terms, however, for the period since 1980, bonds narrowly beat stocks as the post-2000 bear market hit shares.

So it’s a case of stocks for the long run, but this doesn’t rule out a lousy decade or two. Indeed, a truly unfortunate investor would have bought Austrian stocks just before World War I. That would have led to 97 successive years of losses. In Britain, the longest stock investors have had to wait for a positive real return since 1900 is 23 years.

Source: London Business School

What now? Note, says the report, that our expectations have been skewed by the strong recent performances of both bonds and stocks. “The high equity returns of the second half of the 20th century were not normal, nor were the high bond returns of the last 30 years.” With bond yields so low (reflecting sky-high prices), prospective real returns over a 20-year holding period will be “firmly negative”.

Low real interest rates aren’t good news for stocks either; they are associated with poor returns over the subsequent five years. Investors demand a higher return from stocks to compensate for the extra risk compared to risk-free bonds or cash. But if bond yields and interest rates are historically low, then stock returns, once the extra return investors demand is accounted for, will be lower than usual too.

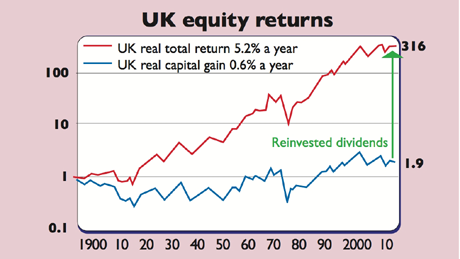

So global stocks may only return around 3.5% a year over the next 20 years, reckons the study. We are stuck in a post-crisis, low-return world, and it could be years before we shake off the post-bubble hangover and interest rates rise significantly. The unusually uncertain outlook makes it all the more important to reinvest dividends. Since 1900 British stocks have risen 316-fold with dividends reinvested – but just 1.9-fold without.