The former basketcase is now in good shape and is cheap enough for a punt, says Phil Oakley.

Margaret Thatcher considered the sale of the postal service a privatisation too far, but the current government does not share her view. Last week, it announced its intention to sell off a stake in Royal Mail during the next few weeks. The Post Office – which runs the post office network – is now a separate company, and is not for sale.

Looking at past experience, apart from the disastrous privatisation of Railtrack, most share sales of state-owned businesses to the public have been kind to those who bought in and held for the long term. So should you sign up for Royal Mail shares – or stay well clear?

What are you buying?

Given that most of us receive letters and parcels on a regular basis, the Royal Mail should be a fairly easy business to understand. The bulk of its business comes from delivering letters and parcels within the UK. It also has a separate European parcels business that gets most of its income from France, Germany and Italy.

Royal Mail is the biggest parcel delivery company in Britain, handling over a billion parcels a year. It is the only mail company that is obliged to provide a universal delivery service to 29 million addresses in the UK for one price. It costs around £7bn a year to run its delivery network.

The business is primed for sale

During the last few years, the government and the company have gone about making the business a lot more attractive to private investors. And it looks as though it is being sold at a very opportune time.

Not so long ago the Royal Mail was a bit of a basketcase. It was a grossly inefficient business that had failed to adapt to the changing ways in which people communicated with each other. The use of the internet and email has seen the number of letters being posted fall year after year.

The growth of internet retailing, which has driven parcel volumes higher even as letter volumes fall, saw rival parcel providers cherry pick lucrative urban areas to take business away from Royal Mail, which was saddled with the high costs and obligation to deliver everywhere in the UK. Customer service also left a lot to be desired.

So a few years ago the Royal Mail set about putting its house in order. It has spent £2.8bn making the collection, sorting and delivery processes more efficient. As a result it is now spending £500m a year less than it would have been if it hadn’t done this.

The government has also been very helpful to the company. Three years ago Royal Mail’s pension fund was over £8bn in the red. Now that problem has been shifted over to taxpayers. Elsewhere, the postal regulator, Ofcom, has stated that Royal Mail must be allowed to make a profit on its universal service obligations. It has said that a profit margin of 5%-10% is not unreasonable. As a result, the price of stamps has gone up. Only 5% of Royal Mail’s business is now subject to regulation, compared with 60% a few years ago.

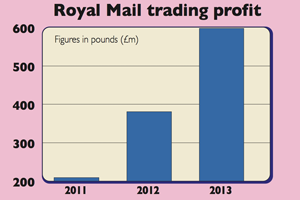

All of this help has seen profits soar in recent years, as you can see from the chart above. A business that was once seeing cash pour out of the door is now seeing lots of it come back in. Debt has dropped and its finances are in very good shape.

Should I sign up for the shares then?

Trading is good at the moment. Parcels – which account for nearly half of the company’s revenues – are booming. Sales were up 13% last year, and 11% during the first quarter of 2013. If Royal Mail is going to grow its profits then its parcels business has to be competitive. If it can look after its customers then the continued growth in internet shopping should see profits go up. Price increases will probably keep profits stable in letters.

One of the key attractions of Royal Mail could be its very strong cash flow, which may allow it to pay some very chunky dividends. Last year it generated £334m of surplus cash, but a look through its accounts suggests that it could do a lot better than this in the years ahead.It spent £665m on investment last year, but this included big redundancy and business transformation costs, which won’t be needed every year. Once these have finished it’s possible that annual investment spending could be half of last year’s level. Cash flow will also get a boost from the lower interest bills that will result from a refinancing of the company’s borrowing.

Last week, Royal Mail said that its annual dividend would be the equivalent of £200m had its shares already been listed on the stock exchange. It would also look to grow it from this level. If its cash flow grows it should be able to do this. The unions are set to throw a spanner in the works by calling a strike over pay and pensions in October. But Royal Mail says it has plans in place to deal with it.

That said, I think the shares will be priced to reflect the concerns that some people will have. City analysts expect the business to float with a value of between £2.5bn and £3bn. If this turns out to be true, the shares will look cheap, trading on just 7.6 times last year’s fully taxed earnings, even at the top end of that range. A dividend yield of between 6.7% and 8% based on a £200m payout looks tempting too, and would sit nicely in a tax-efficient Isa (individual savings account) or Sipp (self-invested personal pension).

Verdict: risky, but cheap enough to buy

The numbers

| Indicated market value | £2.5bn to £3bn |

| P/e ratio (based on latest profits) | 6.4 to 7.6 times |

| Dividend yield | 6.7% to 8% |

| Dividend cover | Two times |

| Net debt (March 2013) | £906m |

| Net assets (March 2013) | £1,405m |

| Gearing | 64.5% |

| Interest cover | 6.3 times |

How to subscribe for the shares

At least 41% of the shares are expected to be sold, with 10% going to employees. This could go up if demand is high. The timetable has not been released yet, but here’s a few things to consider.

- Register your interest with your stockbroker, then apply via them.

- Alternatively, apply direct to the government at www.gov.uk/royalmailshares.

- The minimum subscription is £750.

- The maximum subscription with a debit card is £10,000. There is no limit with cheques.

- You might not get all the shares you want. You may get none at all, depending on demand, although it does seem likely that more shares would be released if this ends up being the case.