Bus and rail company shares can be difficult to weigh up because rail franchises don’t last forever. A firm could see a big part of its profits disappear if it loses one.

When valuing the shares, you need to work out how much the bus and rail businesses are worth separately. It’s also worth seeing if the dividend can be paid out of its more reliable bus profits. FirstGroup (LSE: FGP) couldn’t do this and had to slash its dividend.

But this company looks interesting. Its three rail franchises run out by the end of 2015 and will contribute little to profits until then. So, essentially it is a bus business for a while.

What attracts me is the strong possibility that these franchises will be extended for another three years and that the bus business could see a big improvements in profits.

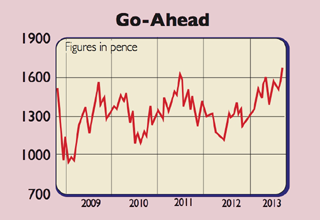

Go-Ahead (LSE: GOG)

The West Coast Main Line fiasco showed that British rail franchising is a mess and the government needs time to sort it out. Franchises due to end are being extended until a credible bidding process can take place. This could be good news for Go-Ahead. Broker Jefferies reckons that three-year extensions with modest profit margins of 4% until 2018 could be worth 139p a share to shareholders.

Go-Ahead’s decent bus business is not doing as well as it should. Management has a plan to get profits from the current £74m to £100m by 2016. It is on track, which means that this business should be worth a lot more in three years’ time than it is today.

Meanwhile, the 4.9% yield can be paid from bus profits, although it probably won’t grow much. The shares are worth buying.

Verdict: buy