The industrial recovery is gaining momentum. A survey of the manufacturing sector, the CIPS/Markit report, pointed to quarterly growth of around 2% between April and June, the fastest pace in 20 years.

In June, activity was just shy of November’s 34-month high. A sub-index measuring job creation in the sector reached its highest level in over three years. Export orders hit a six-month high.

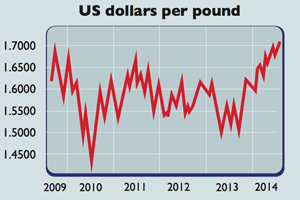

The manufacturing data implies overall GDP growth of almost 1% per quarter, according to Alan Clarke of Scotiabank, making an interest-rate hike before Christmas more likely. The pound rose to a six-year high of around 1.72 US dollars.

What the commentators said

So far, industry has coped well with the strength of sterling, said Larry Elliott in The Guardian. “Whether it would continue to do so if the pound appreciated by a further 10% is questionable.”

It hardly helps matters that businesses on the other side of the channel don’t sound nearly as optimistic as their British counterparts. There are indications that the weak recovery in Europe, which accounts for about half of UK trade, is petering out, which will undermine exports.

It’s great news that manufacturing is rebounding fast, but it still has a lot of ground to make up, noted Philip Aldrick in The Times. The sector shrank by 13.3% from the 2008 peak, and it’s still 7% smaller than it was then. It has also been in structural decline for decades: today it comprises 10% of national output, down from 20% in 1995 and 36% in 1948.

So while manufacturing is now powering ahead, talk of rebalancing the economy away from consumption and towards “George Osborne’s feted ‘makers’” is overblown, said Aldrick.

If manufacturing were to grow its share of national income, it would have to grow faster than the overall economy for several years. That implies an annual growth rate of around 4%. The best it could do between 1997 and 2007 was 2%.

Still, at least the economy isn’t as skewed towards consumption as it was pre-crisis. Ed Conway, also in The Times, pointed out that business investment has been rising for five successive quarters. And households’ debt-to-income ratio has fallen to a ten-year low of 140%. Six years after the crisis hit, the repair job is making slow but steady progress.