A good way to make money from shares is to invest in what are known as turnarounds. These are companies that have got themselves into trouble and are looking to get out of it by following a plan of action. The shares of troubled companies initially get hammered when there is bad news, but can soar if profits eventually recover.

This can often be a better investment strategy than buying quality blue-chips, but it comes with significant risks if the turnaround plan fails.

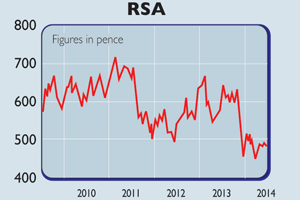

This insurance company, which fits into this category quite well, sells its insurance products under the brand name More Than. The share price of RSA Insurance Group (LSE: RSA) was hammered by an accounting scandal in its Irish business, which led to its dividend being scrapped.

The company had to go cap in hand to its shareholders for more money – a hefty £773m – to shore up its finances. Stephen Hester – the man who tried to fix Royal Bank of Scotland, with some success – has been brought in to get the company back on an even keel.

He’s cleaning the company up by slashing costs and selling off smaller overseas businesses. He’s also getting out of less profitable insurance contracts – in areas such as car insurance – so that RSA can focus on what it does best.

The company makes good money in places such as Scandinavia and Canada and has decent growth prospects in Latin America, but it really needs to do better in the UK.

RSA’s share price has stabilised in recent months, but is still 25% lower than it was a year ago. Insurance is a very competitive business and investment returns are low, so Hester will have his work cut out to get RSA’s profits growing again.

In the short term, profits will go down before they go up. However, Hester stands to pocket a lot of money if he can turn RSA around.

If his strategy succeeds, then RSA will be a much better and less risky business. After losing money in 2013, RSA is targeting a return on shareholders’ equity of between 12% and 15% over the medium term.

That would be a decent result. Shareholders won’t see much of a dividend in 2014, but could see a big increase in dividend payments to over 20p per share by 2016 if Hester’s plan works – that would give a yield of about 4.3% on the current share price.

RSA’s shares are not deeply depressed at the moment. At 468p, they trade at 1.14 times their expected book (net asset) value of 410p. Rival Aviva trades on 1.6 times.

If RSA becomes less risky and its book value gets bigger, there’s a decent chance the stock market will put the shares on a higher multiple of book value. If so, you could make money by buying the shares at 468p – as long as you are prepared to be patient.

Verdict: worth a punt