It’s often said that profit warnings come in threes. If that’s true, you probably won’t be thinking of buying shares in Leeds-based Dart Group (LSE: DTG), as it issued its first warning last month.

The company owns budget airline Jet2.com and Jet2holidays, as well as a logistics business distributing prepared meals to supermarkets. Logistics doesn’t make much money for Dart, so investors should focus on the future potential of its airline and packaged holiday business.

The company is led by Philip Meeson, a charismatic former RAF pilot who occasionally courts controversy with his plain speaking. Back in 2009, the police were called to Manchester airport after he lambasted his staff for not dealing effectively with a passenger queue.

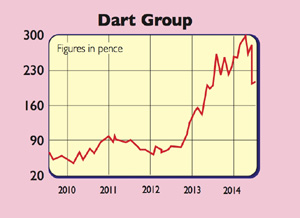

Last month he announced that Dart Group did very well last year. It doubled the number of package holidays it sold, while the Jet2.com airline’s profits increased by 17% to £31.2m.

But that’s where the good news ended. Sadly, Meeson said that things weren’t going so well this year and he expected profits would not meet market expectations. Analysts didn’t like this and predicted that earnings per share would fall by a third to 16.6p. The shares tanked by almost the same amount and have not recovered.

Investors often feel that profit warnings are an act of betrayal and head for the exit. Sadly, they are just a fact of business life. They can throw up decent opportunities for bargain hunters if there’s a chance that profits will bounce back.

Dart’s business model is based on selling package holidays and flights from airports across the north of the country. It has grown rapidly in recent years and now has a fleet of 55 planes. It’s seeking further growth by expanding the number of destinations it flies to – think sunny Mediterranean resorts and popular European cities.

The risk with travel and airline companies is that they put too much capacity onto the market and have to slash prices to fill it. Bigger companies, such as TUI Travel and Thomas Cook, have made this mistake. However, Dart has done well so far. It’s kept its planes full (91% load factor) without slashing prices.

Analysts expect Dart’s earnings per share to bounce back to over 25p in two years’ time. At 208p, that would put the shares on a price-to-earnings ratio of 8.3 times. These shares are not for the nervous, but could be worth a punt.

Verdict: buy