The last decade has been a mixed blessing for investors in emerging markets. Taken over the whole ten years, to June 2014, emerging markets have comfortably beaten developed markets: the MSCI Emerging Markets index had an annualised total return – including reinvested dividends – of 12.3%, in US dollar terms, compared with 7.84% for the MSCI World index of developed markets.

But gains in the second half of that period were very disappointing compared to what had gone before. During the last five years, annualised returns of 9.58% for emerging markets lagged a long way behind the 15.62% managed by developed economies. So which half of the decade was normal – and what can we expect for emerging markets in the future?

A look at the long term

Tracking emerging-market returns over the long term is difficult due to lack of historic data, since the first broad emerging-market indices such as the MSCI Emerging Markets were only created in the 1980s and 1990s. But Elroy Dimson, Paul Marsh and Mike Staunton, of London Business School, have constructed an index backdated to 1900, based on what would have been considered major emerging markets at each point in time.

According to this index, the annualised return from emerging markets between 1900 and 2013 would have been 7.4% in US dollar terms, versus 8.3% for developed markets. In other words, contrary to what most investors believe, developed markets appear to have beaten emerging markets over the very long term.

This makes the case for investing in emerging markets look very weak. But does it reflect what we can expect from emerging markets in the future? Probably not. Their poor performance largely reflects events in the first half of the 20th century, when revolution and war meant that investors in many emerging economies, such as pre-revolutionary China and Russia, lost everything.

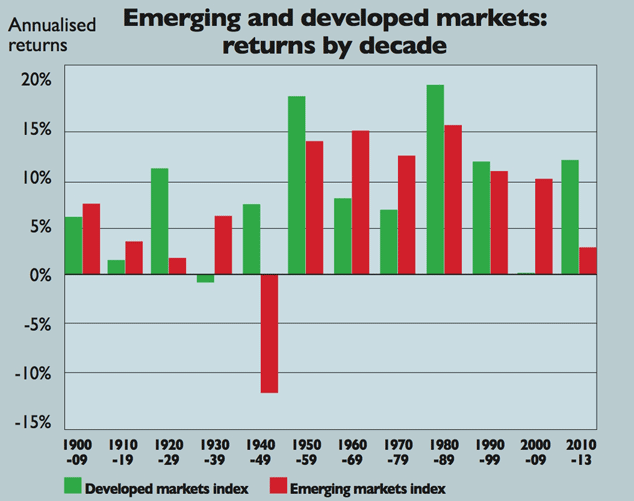

In the more stable conditions that prevailed from 1950 to 2013, emerging markets did rather better, returning 12.5% versus 10.8% for developed markets.

However, as the chart above shows, emerging markets still lagged behind developed marketsin half the decades since 1950. And their outperformance since 2000 was unprecedented by historical standards. This clearly shows the importance of taking a longer-term view and having realistic assumptions about the returns emerging markets are likely to deliver.

Diverging markets

That said, while emerging markets as a whole haven’t done as well as hoped lately, that certainly hasn’t applied to all cases. Over the last few years, returns have diverged much more than many investors realise.

For example, the MSCI Philippines index had an annualised total return of 24.49% in US dollar terms over the last five years, comfortably outperforming both the MSCI Emerging Markets and the MSCI World.

Other southeast Asian markets such as Thailand (19.89%), Malaysia (16.34%) and Indonesia (15.53%) have also seen strong returns. Conversely, other emerging economies such as Brazil (2.47%) and Chile (3.85%) have lagged far behind.

The same is also true at the stock and sector level. Many emerging-market consumer stocks have performed well even while the broader indices have fallen behind.

For example, the MSCI Emerging Market Consumer Staples Index had an annualised return of 17.88%, in US dollar terms, over the past five years. So even during a very weak spell for emerging markets, there have been opportunities to earn good returns.

The importance of value

Of course, that doesn’t mean the markets that have performed best in recent years will continue doing so. Past performance is not a good guide to the future and last year’s star is often next year’s laggard.

Indeed, one reason that emerging-market returns sometimes disappoint is that people get carried away by exciting growth stories and end up overpaying for them.

Many investors are surprised to discover that focusing on value is as useful in emerging markets as it is in the developed world. A recent paper by Matthias Hanauer and Martin Linhart, of Technische Universität München, found that value stocks outperformed growth ones in emerging markets by an average of 0.93 percentage points per month over the period from 1996 to 2012.

At a country level, Dimson, Marsh and Staunton found that countries with the highest trailing dividend yield outperformed the lowest yielders by 19 percentage points per year on average, over the period from 1976 to 2013.

They also found that investing in countries with the highest growth over the past five years – as investors will often do if they give too much weight to the recent past – delivered worst returns, while those with lower historic growth substantially outperformed.

The good news is that many emerging markets look relatively cheap. The MSCI Emerging Markets index trades on a price/earnings ratio of 13, compared to 18 for the MSCI World. That implies that emerging markets could well be set to outperform developed markets over the medium term. But investors should be aware that the exceptional returns of the early 2000s are unlikely to be repeated.