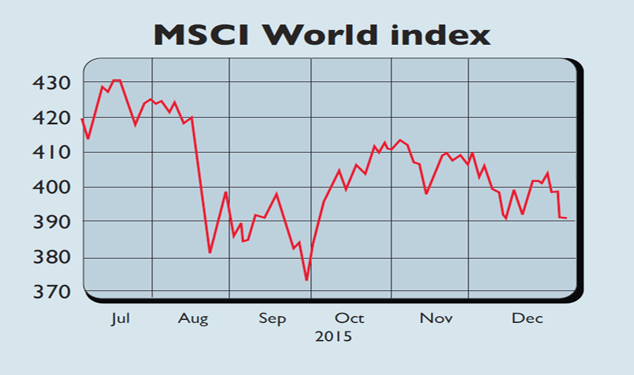

Talk about a New Year hangover. By mid-week, the MSCI World index tracking both developed and emerging markets had lost 2.5% and hit a three-month low. Monday saw several markets suffer their worst first trading day in years; the pan-European DJ Stoxx 600 index had its worst on record.

Brent crude futures have slumped to under $35 a barrel, a 12-year low. Emerging-market stocks fell to a new post-crisis low and emerging-market currencies followed. North Korea’s claim to have tested a hydrogen bomb unsettled investors already worried about mounting tension between Iran and Saudi Arabia.

What the commentators said

“This is… a replay of the same things that moved the markets in August,” said Benjamin Dunn of Alpha Theory Advisors. Last summer the shock devaluation of the yuan sparked a global sell-off. This week the Chinese central bank set the currency’s daily reference rate at an unexpectedly weak level, allowing the currency to decline to a five-year low. That reawakened fear that China is struggling to bolster growth, while a plunging yuan could export deflation.

China’s weakness has dragged down commodities too, which means that “the turn of the calendar will not alleviate pressure” on raw materials exporters and emerging markets in general, said Brown Brothers Harriman. It hardly helps that investors have been turning their back on the sector in anticipation of higher interest rates in America, which always make riskier assets less appealing.

Meanwhile, oil’s initial uptick amid the Iran/Saudi row has rapidly dissipated as the focus returns to the huge glut in the oil market. The market is interpreting the tension as bearish “as it means [there] is even less chance of an Opec agreement”, said PVM’s Tamas Varga. Absent an Opec consensus to stop pumping at full throttle, Saudi is not going to cut back and thus help Iran gain market share.