This week I feel a bit embarrassed. Some readers might remember an article I wrote some years ago about buying a large house in Edinburgh. It was, I said at the time, likely to be one of the worst financial decisions ever, but my family needed to nest — so we wanted to own a house.

It hasn’t turned out to be completely awful. We could probably sell it for roughly what we bought it for in nominal terms. So we are only down about 15% in real (inflation adjusted) terms. I’ve made worse decisions. So that’s not the embarrassing bit – this is: we just bought a tiny studio flat in London. When I say tiny, I mean tiny. The entire thing is around the size of our family bathroom up north.

But still, given my firm and often expressed view that London property is hideously overvalued, you’ll be wondering what on earth I am thinking. The answer, once again, is domestic. I travel up and down the east coast of the UK like a yo-yo. I need somewhere to leave my “giving a talk” clothes and heels that isn’t the lost property department of Virgin East Coast rail, and somewhere to sleep when I miss the last train to Scotland. It’s a utility purchase I intend to depreciate over 20 years, not an investment.

I’m telling you this dull stuff about my personal life not, sadly, because I think you will be particularly interested, but because the rest of this article is about the London property market and I want to pre-empt a Twitter row about why I don’t follow my own advice. I’ve just told you why. So, onwards.

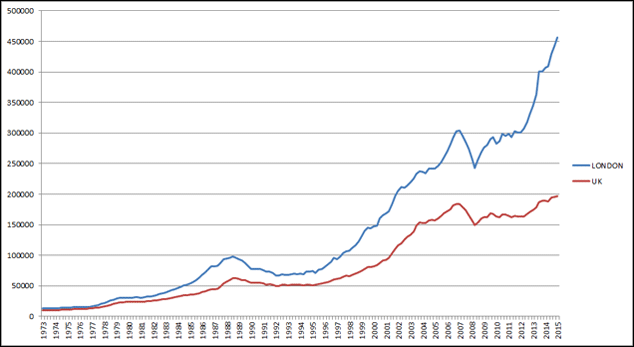

Source: Nationwide

Here’s a chart showing the relationship between average London house prices and those in the rest of the country. You’ll see a pretty clear cycle. The gap widens. Then it reverts to around the mean. Then it widens. And then it reverts. Today it is wider than it has ever been: the line showing London prices soars up, up and away.

There’s a clear message in there for anyone who believes in reversion to the mean: sell your house in London and buy one in the country. But this chart isn’t the only thing sending that message. There is also the basic economic truth about demand creating its own supply. You’ll have heard a lot of talk over the years about how it isn’t possible to substantially raise the supply of housing in London. But a PropertyVision report out this time last year proved that to be nonsense: it noted that “the sheer scale and monumentality of the towers that are rising daily is in a league of its own” and counted 54,000 new flats on the way in central London.

Anyone who keeps an eye on planning applications — or for that matter the Homes & Property section of the Evening Standard — will know that number has been rising steadily: there are 10,000 new flats planned on public land around Wormwood Scrubs, for example. Transport improvements are also making areas once thought of as outer London as commutable as parts of central London — something that Crossrail will do even more to emphasise.

So we have a price signal here (too high) and we have a supply signal (lots coming) too. Next up is a policy signal. The government is not keen on super high house prices in London. It looks bad. So they have been working to discourage foreign buyers with the higher stamp duty rates and the annual tax on enveloped dwellings (Ated) for houses bought inside companies. They also hit the market with the new rates of stamp duty for houses worth £1.5m plus and told us that anyone buying a second home would be paying 3% extra from April.

London used to be lightly taxed by international super city standards. Add the nasty cuts in tax relief on buy-to-let interest and it clearly isn’t any more.

That’s three signals for you. The fourth comes from the market. London has long been a lovely haven for international buyers. But with commodity prices collapsing and China slowing, the bread and butter of the high-end market isn’t as well off as it was: no Russian oil billionaires are going to spend £60m on a penthouse apartment in Hyde Park this year. Quite the opposite: I’ve already heard of several massive price cuts from “distressed sellers”. The great unwinding of the global credit bubble can take London houses down with it just as easily as it can take steel mills.

The fifth is obvious — interest rates. The base rate in the UK remains 0.5%. According to the Taylor Rule (a pretty well accepted monetary policy rule that suggests what interest rates in any one country should be) it should be 4.2%. Yikes. Add it all up and the future for London house prices really seems very clear. Crash. Crash. Crash. And a few extra sleepless nights for me in my cramped and airless little studio.

But here’s the thing. I can’t be absolutely certain on all this. One of the things I missed in the post-crisis period was just how global a market London is. So it makes sense to look at prices in currencies other than sterling. Do that and prices haven’t budged much since 2011: a friend who bought then in Notting Hill reckons he is just about even in dollars. Foreign buyers will see London as more taxed than it was, but not necessarily more expensive.

I’m also unnerved by the Swiss question. FT readers will have seen the story earlier in the week about the tax authorities there urging people to withhold their payments until the last minute. Why? Negative interest rates mean they don’t want to hold the cash — they want the taxpayers to take the hit instead. If the current market corrections turn into full-blown chaos, we know what central banks around the world will do. Taylor rule be stuffed, they’ll cut rates and print money. And if they do that no one will want cash. We will all move into more and more risky investments to avoid having it — London property could still be one of those investments.

If I had £4m to buy a house in London now would I buy one? No. Absolutely not. No way. And, just to be clear, if I wasn’t long-distance commuting, I wouldn’t buy a studio either. But at least thinking about the increasingly bonkers nature of the global economy gives me a straw to grasp at, given that I have.

As does this idea: if people are moving out of London to buy gorgeous houses in Suffolk and Somerset but are still working in London, what will they need? Studios. Perhaps the reversion to the mean caused by people selling big houses in Notting Hill will also mean a bull market in tiny studios. Here’s hoping.

• This article was first published in the Financial Times