With the average car-insurance policy costing £760 a year, according to Confused.com, insuring a vehicle that is parked most of the day is a poor use of your money. In fact, many cars spend more than 90% of their time entirely static, says the BBC. However, a new approach to insurance may be the solution to this problem: pay-as-you-go car insurance could mean you now only have to insure your car when it is actually on the move.

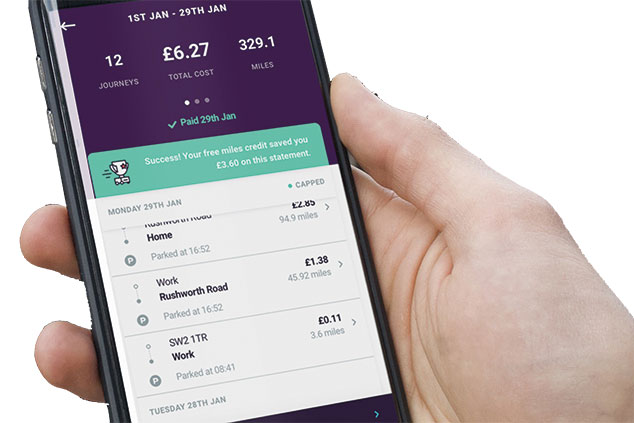

By Miles is a car-insurance firm that uses a black box to monitor its customers’ journeys, and then charges you per mile for insurance. You pay a fixed fee to cover your car for fire and theft for the whole year – so it is covered if something happens while it is parked – but then you pay the rest of your premium as and when you use your car.

Pay-as-you-go insurance is “designed for motorists who travel under 7,000 miles a year or 140 per week in their cars”, says Luke John Smith in the Daily Express. “Essentially, the less you drive, the lower your insurance is, but rates will vary based on the model of car, its age, where it is parked and the driver’s experience.”

The BBC gives the example of John Leahy who lives and works in London, commuting on the Underground. He only drives around 4,000 miles a year. Leahy estimates that he will save between £100 and £150, or around 20% of his annual premium through using By Miles. This year, he paid a £170 fixed fee and a £50 deposit, and will then owe 3.4p for every mile he drives. At the end of each trip, he gets a notification telling him how much it has cost. “I’m now of the mindset of thinking, ‘Do I need to take the car?’”, Leahy told the BBC. “Because not only will I be paying for the petrol, but I’ll also be paying for the insurance.”

Just keep in mind that to benefit from this by-mile insurance, you have to be happy to have a tracker installed in your car to allow the company to monitor how far you travel and charge you accordingly.

It’s also worth being aware that you can get insurance charged by the hour instead, but this is mainly geared towards people wanting to drive a friend’s car without having to get their friend to add them to their own policy.

Some better-known providers are Cuvva, Tempcover and Veygo – with Cuvva, one hour’s insurance costs, on average, £10, with three hours setting you back by slightly more than £13.

Avoid credit complacency

When was the last time you checked your credit rating? Most people assume that as long as they haven’t been made bankrupt or defaulted on a payment, and have avoided debt, they have a good credit score. In fact, even if you have never made a financial mistake, you can still be rejected when you make an application for a credit card or loan.

Up to 5.8 million people are “financially invisible” because they have little or no information on their credit history, says credit-reference agency Experian. So when they do apply for credit, they are likely to be rejected, as lenders are unable to tell how likely the applicant is to pay back debts. Alternatively, they may be approved for a loan, but offered a much higher interest rate than the one advertised.

The problem affects the full wealth spectrum, not just those on lower incomes. If you are planning on applying for credit – whether that’s an overdraft, credit card, loan or mortgage – it’s worth checking your credit report first. If you have a low rating, then you can improve it by making sure you are on the electoral roll, getting a mobile-phone contract, and taking on a credit card (repaying the full balance every month).