This article is taken from our FREE daily investment email Money Morning.

Every day, MoneyWeek’s executive editor John Stepek and guest contributors explain how current economic and political developments are affecting the markets and your wealth, and give you pointers on how you can profit.

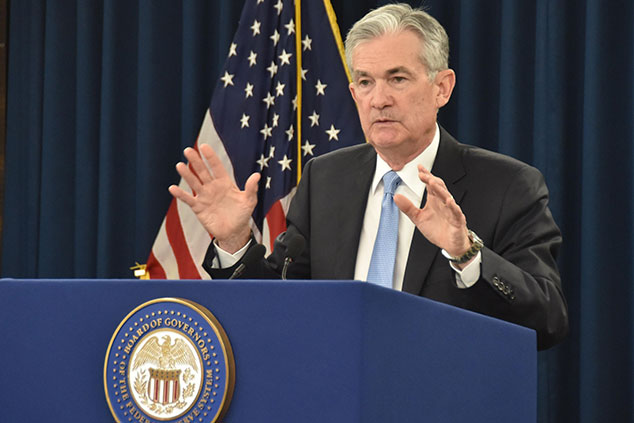

The Federal Reserve, America’s central bank, delivered its latest decision on monetary policy yesterday.

The Fed is now clearly worried that it has done too much tightening already.

So it was very much back to business as usual – surprise the market by being even more “dovish” than expected.

The question is: will it be enough?

The end of quantitative tightening is nigh

The US central bank is by now well-known for keeping a close eye on the stockmarket’s reaction when it sets monetary policy.

This was christened the “Greenspan put” back in the days when Alan Greenspan was in charge. The belief was that you didn’t need to worry too much about the downside in markets, because the central bank would always be ready to cut interest rates if stocks fell too far and too fast.

So far that has broadly proved to be the case. The “put” was maintained, following the financial crisis, under Ben Bernanke and Janet Yellen. The belief in its existence was shaken under new chairman Jerome Powell during 2018.

But at the start of this year, he did a U-turn. And now he’s making sure that the market knows that he has its back.

So what came out of the latest meeting? First things first, the Federal Reserve doesn’t expect to raise interest rates again this year. And it only expects to raise them once by the end of 2021.

Just a few months ago, the expectation was for two rate rises by the end of 2019. So this is a big shift in the direction of much easier monetary policy. (Although it’s worth noting that the market is now starting to price in a cut in rates for next year.)

More importantly, the Fed has outlined when it will call a halt to quantitative tightening (QT – the process of reversing quantitative easing). It will be doing less QT from May, and it will stop altogether in September.

In other words, the Fed is going to stop taking money out of the financial markets, which is one of the key things that rattled markets so badly towards the end of last year.

From then on, the plan is that the Fed will keep getting rid of its mortgage-backed securities, but that it will replace those with US Treasury bonds. In other words, it will just be swapping one for the other, rather than taking money out of the system.

Why aren’t markets happier?

This is what markets want to hear. They want a dovish Fed. Yet they didn’t exactly roar ahead. Yes, the S&P 500 rallied at first, but it couldn’t hang on to the gains by the end of the day.

Clearly markets are rattled that Powell really does know something that they don’t, and that a full-on slump is around the corner. And it’s true that the most recent economic data from the US doesn’t look great.

Equally, there are the ongoing jitters over the US trade war with China to contend with. Murmurings that there might not be a deal after all (which seem to amount to little more than the usual gossip and chit-chat) helped to unnerve investors towards the end of the session.

But the other big issue is bond yields. The idea that the Fed will be buying more Treasuries later in the year helped to drive the price of US government bonds sharply higher, which means that yields fell. But this is also what you’d expect to see if investors are becoming more worried about the state of the economy.

The yield on the ten-year US Treasury is now at its lowest level in a year. This does not indicate optimism about the outlook. It does not suggest that investors expect inflation to take off any moment now. Indeed, it indicates that investors reckon the economy has already peaked.

Another problem with falling bond yields is that – at these levels – it is not very healthy for the banking sector (it’s a longish story, but the upshot is that it makes them less profitable).

And, like it or not, banks are still an important part of the economy. If banks are struggling, then they won’t be lending, and if they’re not lending, then it’s harder for businesses to expand and grow.

This does rather indicate the problem with having interest rates so low for so long. You can argue about the direction of the causation until the cows come home. But there is a risk that your economy becomes mired in quicksand.

Ultra-low interest rates interfere with the process of efficient capital allocation (which is the fundamental point of free markets). You get overcapacity across the board because no one is going bust. As a result, you bake deflation into your economy, because as soon as you withdraw monetary support, you run the risk that this overcapacity causes a collapse.

Of course, this could also all be a scare. These things feed off each other. Markets are worried because they think the Fed knows something they don’t. The Fed is worried because it doesn’t want to cop the blame for being too slow to react if this does turn into a recession.

What’s the upshot? Watch and wait. And keep an eye on the dollar. Of all the “risk-on, risk-off” indicators, this is the trend that matters most. And certainly, the Fed’s actions should make for a weaker dollar, all else being equal.

So stick to your plan. Invest in good value markets, and own some gold. And if you haven’t already subscribed to MoneyWeek, do so now and get your first six issues free.