The supermarket faces tough challenges – so should you wait for a better time to buy? Phil Oakley investigates.

For years it seemed that Tesco could do no wrong. Loved by its customers and the City, it dominated British food retailing and set its sights on becoming a global giant.

Under the leadership of Sir Terry Leahy, Tesco built up a huge land bank and set about smothering the country with supermarkets and local convenience stores. It also launched a substantial online grocery business and branched out into areas such as banking and mobile phones. The company led the way with keen pricing and its innovative Clubcard loyalty scheme.

So why have things gone so terribly wrong for Tesco since Sir Terry decided to bow out just over three years ago? Philip Clarke, his successor, has had a horrible time as profits have fallen and the company has lost market share. Now Clarke has stepped down and Tesco is turning to a man called Dave Lewis. Lewis comes from consumer goods company Unilever and has a reputation for doing good things. Investors will be hoping that he can restore Tesco to its former glories.

Can Tesco be fixed?

There weren’t many naysayers on Tesco during its heyday. However, back in the early 2000s when I was a food retail analyst at an investment bank, I worked with one. My colleague, an analyst with a keen eye for detail, was sceptical about the quality of Tesco’s profits and the ability of its overseas stores to make decent returns on the investment it had made in them.

Management from rival retailers believed that Tesco’s perceived success was largely down to its huge building schedules. A steady stream of new supermarkets getting up to speed gave the impression of strong underlying sales growth, when in reality it probably wasn’t that impressive.

How times have changed. Tesco’s pursuit of size may have sown the seeds of its current woes. It was lucky that it did not have many strong competitors to stand in its way in the past. Ten years ago, Sainsbury’s and Morrisons were in a mess, while Waitrose and the German discount stores didn’t really have a meaningful presence. With the exception of Morrisons, that’s not true now.

A lot has been said about the damage that cheap supermarkets such as Aldi and Lidl are doing to the likes of Tesco. Their lower prices are certainly wooing shoppers, but Tesco’s problems are more deeply rooted than this.

Tesco’s chief problem in the UK is that it is too big. It has also lost touch with its core customers and is no longer giving them what they want. This is not going to be fixed by clever marketing spin, it needs something a lot more radical.

Britain has too many supermarkets. The industry is subject to the basic rules of demand and supply. Over the last ten years we have seen a big increase in supply, which, unsurprisingly, has ended up with too many stores chasing too few customers. That’s meant lower profits for most of the big players. Tesco has more to lose than most, having splurged on big out-of-town stores to sell the stuff that people now buy on the internet.

Getting out of this mess will not be easy. Tesco has effectively remortgaged a lot of its big stores and is renting them back from property companies – meaning that it has around £11bn of hidden debt. Tesco has break clauses on some of these leases, but any such break will incur a penalty fee. According to the annual report, ending all those breakable leases would cost £5.4bn – money Tesco probably doesn’t need to spend just now.

Arguably the best strategy for Tesco is to break itself up. It could slash prices and take on the competition with a core network of stores and then focus on creating a big online retail business.

It seriously needs to consider getting out of a lot of its overseas markets – such as eastern Europe – where profits have

fallen sharply. This would create havoc with its finances in the short term and would probably lead to much lower profits, huge write-downs on the value of its properties and a dividend cut. However, the strategy might pay off in the long run as it could make life very difficult for competitors.

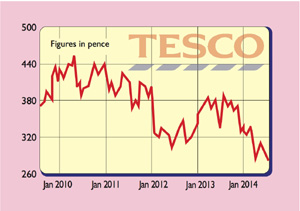

The trouble for existing and potential investors in Tesco is that it’s difficult to work out how far profits can fall and at what level they become sustainable again. My guess is that profits could fall a long way from where they are now, even after analysts have slashed their forecasts.

At the moment, analysts are expecting Tesco’s trading profits to stay flat at around £2.9bn for the next three years. This looks optimistic. Last year its UK supermarkets had profit margins of 5% on sales of £43.6bn. It’s obvious that Tesco needs to cut prices, so we might see a 4% profit margin soon. That would imply a 15% fall in profits if sales don’t respond to the price cuts. That means the prospective price/earnings ratio of 10.8 and dividend yield of 5% need to be taken with a big pinch of salt.

Lewis may bring some much needed fresh thinking to Tesco, but he has taken on a very hard and painful job. Tesco could recover, but things may have to get worse before they get better. Now is not the time to buy the shares. Patient investors may get a better entry point.

Verdict: one for the watch list

The numbers

Directors’ shareholdings

P Clarke (CEO) 1,977,807

L McIlWee (CFO) 84,688

R Broadbent (Chair) 63,996

What the analysts say

Buy 12

Hold 15

Sell 12

Target price 300p

Key facts

Stockmarket code LSE: TSCO

Share price 279p

Market cap £22.7bn

Net assets (Feb 2014) £14.7bn

Net debt (Feb 2014) £6.6bn

P/e (prospective) 10.8 times

Yield (prospective) 5.0%

Interest cover 4.5 times

ROCE 11.0%

Dividend cover 1.9 times