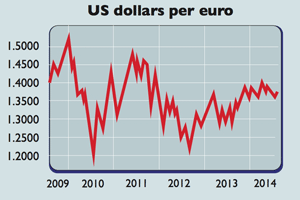

In the past few years, the US dollar has struggled against the other major currencies. The dollar index, which tracks its performance against that of its key trading partners’ currencies, has been treading water for three years. Against the pound, the dollar has slid to a six-year low. It is not far off a three-year low against the euro.

A currency’s strength usually boils down to expectations for growth and interest rate changes, says Ben Levisohn in Barron’s. Solid growth implies higher interest rates. That raises the yield on a currency, making it more appealing.

On this view, the dollar should be doing better than its rivals. The US economy may have shrunk at an annual pace of 2.9% in the first quarter, but that was down to the unusually cold winter.

Deutsche Bank expects American growth of around 3% for the rest of 2014, and the backdrop is promising. Consumer confidence is at its highest level since before the credit crisis. Manufacturing and service-sector activity is strong.

Government spending cuts and tax rises, which have squeezed growth in recent years, are easing up. Even business investment – so far the missing link in this recovery – should start to rise soon, reckons Deutsche Bank.

In turn, this suggests that inflation is likely to rise faster than the US Federal Reserve expects, while the unemployment picture is also likely to improve more rapidly. And that means interest rates may rise sooner than markets currently believe. The US central bank could start to lift them as early as June next year.

Meanwhile, the European recovery remains tepid and the European Central Bank is far more likely to start printing money than to raise rates. The Bank of Japan is also ready to do more quantitative easing (money printing) to weaken the yen and beat deflation.

Only sterling is in a similar position to the dollar in terms of interest rate and growth expectations. But in the pound’s case, a lot of the good news is already priced in, says Morgan Stanley – this is clear from its recent upswings.

All this means that the US dollar is now the horse to back in the currency markets. Morgan Stanley sees the euro-dollar rate easing from $1.37 to the euro to $1.27 by the end of March 2015, and Bank of America Merrill Lynch takes a similar view.