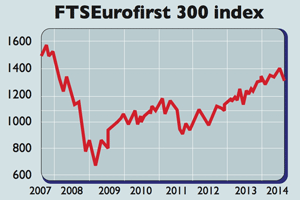

“Investors are losing faith in Europe,” says Manish Kabra, of Bank of America Merill Lynch. Germany’s DAX index has lost 10% from its recent high. Italy’s main market is down 9%; the French CAC 40, down 15%.

Worries over Ukraine have been one factor. But the key problem is an old one: Europe “produces no growth”, says Didier Saint-Georges of fund group Carmignac.

The eurozone’s recovery seems to have ground to a halt. After growing by 0.7% in the first quarter of 2014, GDP was flat in the second. For once, it wasn’t the troubled ‘periphery’ causing the most worry. Portugal and Spain grew by an annualised 2.6%. “Even Greece seems to be on the road back from Hades,” says Hugo Dixon on Reuters.

But in France, where manufacturing and services activity is falling, output was stagnant. In Italy, a renewed slide in GDP in the second quarter was depressing but not surprising, as we noted last week. But the eurozone powerhouse, Germany, which accounts for 25% of the zone’s GDP, also saw output fall.

One problem is the strength of the euro, which is hampering European exports. Italy and France are dragging their feet on economic reforms designed to boost growth, while nervousness over the crisis in Ukraine is starting to dent business confidence, notably in Germany.

High private and public debt loads accumulated before and during the crisis are also still a problem. And now inflation, running at anannual rate of just 0.4%, could go negative.

Falling prices and negligible growth “are a potentially lethal combination for countries weighed down by debt”, says The Economist’s Graphic Detail blog.

The real value of debt rises, making the burden heavier and further denting confidence, investment and borrowing, raising the spectre of a Japan-style slump.

Given all this, the European Central Bank (ECB) is expected to have to resort to quantitative easing (QE – money printing) to ward off deflation and weaken the currency.

QE’s impact on growth may be questionable, but it does give stocks a lift as the printed cash finds its way into markets. This suggests that eurozone stocks remain worth buying. The Greek market remains among the world’s cheapest, on a cyclically adjusted price/earnings ratio of just four.