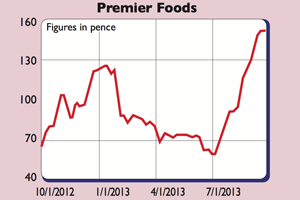

Shares in Premier Foods (LSE: PFD) have soared. They’re up by nearly 70% since I tipped them in March, and by nearly 130% in the last year. This performance proves that taking big risks can lead to big rewards in the stockmarket.

Premier Foods is still a very risky investment. It has little pricing power with the big supermarkets, debts of nearly £900m, and a pension-fund deficit of £300m. Contrast this with the market value of all its shares of just £364m.

But things are getting better. It is selling more of its key brands, such as Oxo, Bisto, Ambrosia and Batchelors, and profits are going up. Problem areas, such as Hovis bread, are being sorted out and more cost savings being found.

However, the company will have to deal with its huge debts eventually and this will probably require a big issue of new shares. Management wants to wait until profits and the share price are higher so it can raise money from a position of strength rather than getting the begging bowl out. This creates a dilemma for investors. Do they hang on in the hope of more gains and a favourable issue of new shares, or do they take profits?

The shares still trade on a low price/earnings (p/e) ratio of 5.8 times, but that’s as it should be because of the risks involved. It would not surprise me if the shares kept on rising, but with Premier still having a lot to prove as a business I’d be tempted to bank some profits now.

Verdict: take profits