I bet that, out of the big four British supermarkets, Tesco will report the strongest like-for-like sales growth this Christmas. That might seem a little contrarian given the firm’s recent woes. So why am I bullish?

Firstly because, although UK sales fell 1.5% in the first quarter (Q1), there are tentative signs that the £1bn turnaround plan – dubbed ‘Build a Better Tesco’ – is beginning to work. Q2 saw like-for-like sales nudge up by 0.1% with its Everyday Value range shooting up 10%, after the grocer recruited 8,000 staff, ramped up promotions, modernised 230 stores and spruced up its fresh meats, fish and bakery counters.

Meanwhile, capital expenditure is being slashed on new hypermarkets. Instead, money is being deployed to expand its smaller Tesco Express format, together with building e-commerce infrastructure such as 90 drive-through, ‘click-and-collect’ points. CEO Philip Clarke says that customers have welcomed the changes, and that its UK business “is on time and on track”.

Secondly, following last year’s bungled £500m ‘Big Price Drop’, expectations for this year are low. The group should easily beat year-on-year UK comparables, especially as Clarke took personal command of the UK division back in March. Let’s not forget too that Tesco still possesses immense economies of scale. Its market share remains at 30%, that’s more than ten percentage points above nearest rival Asda.

Its leadership in web and convenience-store retailing provide it with huge strategic advantages. So successful is the online concept that it is also being rolled out in Prague and Warsaw, and has just launched in Bratislava. Next year is likely to witness a resurgent Tesco looking to make up lost ground.

Clarke certainly has challenges ahead. In South Korea profits are set to dip £100m this year, following a decision by the government to ban Sunday trading for two weekends a month, and restrict opening hours to between 8am and midnight on other days.

Meanwhile, in the US, the troublesome Fresh & Easy chain is still losing money – albeit sales were up 5.2% for the first half year and more stores became cash-flow positive. But I’m not the only one who thinks the Tesco tanker is turning around. US investor Warren Buffett has snapped up a 5.1% stake, encouraged by the 4.5% dividend yield and the cheap valuation of ten times earnings.

Tesco (LSE: TSCO), rated a BUY by Cantor Fitzgerald

The City is predicting turnover and underlying earnings per share (EPS) of £66.3bn and 32.7p respectively for the year ending February 2013, rising to £69.3bn and 34.5p 12 months later. On this basis, I rate the stock on a ten times earnings before interest, tax and amortisation (EBITA) multiple. Adjusted for net debt of £7.2bn and a £1.8bn pension deficit, that suggests an intrinsic worth of 365p per share.

Overall, I think Clarke is doing a good job, and the group’s value credentials should help it during a period where consumers increasingly use the internet and trade-down to cheaper options. Cantor Fitzgerald has a price target of 443p per share and the Q3 trading statement is scheduled for 5 December.

Disclosure: I own shares in Tesco.

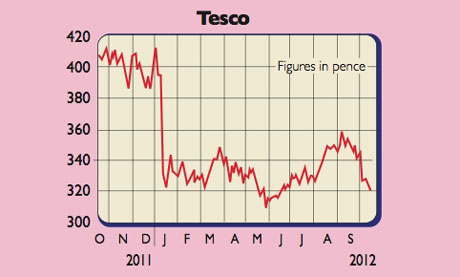

Rating: BUY at 315p

• Paul Hill also writes a weekly share-tipping newsletter, Precision Guided Investments. See www.moneyweek.com/PGI or phone 020-7633 3634.