This article is taken from The Week In Preview published on 15 August by Charles Stanley Stockbrockers

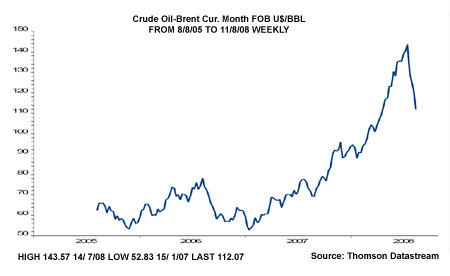

In the UK, dire CPI of 4.4% was well ahead of the consensus expectation of 4.1% and is more than double the MPC’s inflation target of 2%, driven mainly by a spiral in food price inflation with meat prices soaring by 16.3% year on year. Although earlier rises in energy and food prices are still flowing through into inflation, both of these effects could begin to unwind in Q4. Not only has the oil price fallen 25% from its July peak, but global wholesale food prices are now falling sharply; wheat, soyabean and corn prices have also fallen by double digit percentages recently. And although manufacturers’ input prices were higher in July than a year ago, they did show some first signs of inflation pressures easing off. The equity market has also taken heart from recent sharp falls in commodity prices.

Nevertheless, the catalyst for these falls is the global economic slowdown and investors still need to take this on board in terms of the outlook for corporate earnings.

In the year to July, the consumer prices index (CPI) increased by 4.4%, up from 3.8% in June. This news was more alarming than expected, with a whole range of items pushing inflation much higher than economists’ consensus estimate of 4.1%. The largest inflationary pressures actually came from food and alcoholic beverages which rose by 12.3%, with meat, bread, cereal and vegetables all showing large upward effects. Transport cost inflation was 8%; household services such as electricity rose by 7.6%; and even furniture, household items and clothing contributed to the inflation numbers. CPI was the highest since records began in 1997 but the longer standing RPI statistics recorded the highest level of inflation (at 5% in the year to July) since 1991 when the measure was 5.5%.

Although these inflation figures are disappointing, there is some hope at hand from falling commodity prices, especially oil and agricultural prices, and there was a flicker of good news in the latest producer prices data for July. There was an unexpected seasonal decline in manufacturing input costs of 0.6% (consensus economists’ predictions expected a 1% rise) in July. This is the first sign of inflationary pressures easing off, though input prices were still some 30% higher in the year to July and manufacturing output prices were 10.2% higher for the same period. Hopefully, the monthly trend on input costs reflects an inflexion point. The oil price was still at record levels in July, so the 25% fall in oil prices over the last month should be translated into a continuing decline in input costs.

Encouragingly, besides oil, other commodity prices are falling and key agricultural commodity prices have collapsed recently. For example, Soyabean prices peaked at the end of June at 1,565 cents/bushel. Soyabean prices are currently 26% lower at about 1,200 cents per bushel. Similarly, the corn price peaked on 30th June at 680 cents/bushel and is now about 450 or 34% lower. The wheat price peaked in March and is currently 50% lower. Possibly, agricultural commodity prices have been influenced by global speculation, though stocks of soyabeans and corn are low and direction of prices remains highly dependent on weather and subsequent crop yields.

A key question will be how long it takes before falling commodity prices are reflected in CPI numbers. At the moment, utility bill increases are still working their way through into the inflation numbers. Assuming commodity prices remain subdued, inflation could peak near 5% in September. But if commodity prices remain on a downward path, CPI could reverse as quickly as it has risen. CPI has risen from 2.2% in January 2008 to 4.4% in July 2008. The rise in inflation has been largely driven by commodities, not by wage inflation, which remains rooted at about 3.5% p.a.

The Bank of England published its inflation report on Wednesday. It now expects inflation of 5% in the coming months, but appears confident that it will fall back to less than 2% in two years’ time at the current level of interest rates. At the same time, the outlook for growth is weaker. The central bank expects broadly flat output over the coming 12 months with a technical recession. The economy is not only going through a ‘cost shock’ from external factors, but is also affected by the credit crises and a housing slump. If inflation behaves as expected, interest rate cuts should be on the agenda for 2009, possibly to stop CPI overshooting on the downside.

In conclusion, the earlier effects of rising energy and food inflation are likely to push CPI up to new records in coming months and possibly top 5% in September. However, the unwinding of these could equally push inflation much lower in 2009. Consequently, the MPC should be in a position to reduce interest rates in 2009. It appears that inflation risks are likely to recede and investors need to get back to assessing the recession risks on equities. A decline in inflationary expectations is very positive for equities but after the good rally from the July lows, the effects of the global economic slowdown (e.g. the sharp slowdown in Eurozone GDP) and the squeeze on corporate profit margins has yet to be discounted.