China’s meteoric growth has come at a price. Farmers have scorched the hills surrounding Beijing black with chemicals. Shanghai is shrouded in lung-busting smog. But for China’s leaders, there is also a major upside to the country’s industrialisation – by herding its population into densely packed megacities, China is increasingly reducing its dependence on oil. America, lumbered with long highways and gas guzzling cars, suffers every time the oil price resumes its climb. The average Chinese city worker, driving a single-gallon car, is frugal by comparison.

Better still, the Chinese learned another valuable lesson from the Americans two years ago. Back then, the president, George Bush, threw his weight behind corn-based ethanol as the country’s alternative fuel of choice. Beijing watched closely as scores of Midwest farmers diverted crops to ethanol production. And the Chinese paid special attention when the price of corn quadrupled to $8 a bushel in the process. With too many mouths to feed, and concerned for China’s food security, the Chinese have chosen an alternative fuel of their own – methanol. As China recovers from the recent slump, a formidable recovery for this out-of-favour fuel is on the cards.

Methanol is a clear, liquid alcohol typically produced from natural gas. However, the Chinese have been generating quality methanol from coal – largely because they have abundant supplies of it. Producing methanol this way is also quite a cheap process – costing under a dollar per gallon – and the technology has been around for a while. “Already taxi and bus fleets in China run on high-methanol blends,” says Chris Mayer in his Capital & Crisis newsletter. “And retail pumps sell low-methanol blends like US gasoline stations sell ethanol blends.” Overall, Chinese demand for methanol is growing by 15% to 20% a year, according to Dave McCaskill of Chemical Market Associates.

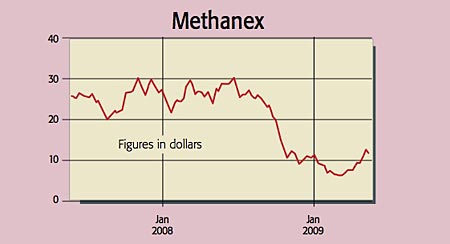

That said, methanol is not a new chemical. You’ll find it in a number of products in your home – from adhesives to paints and plastic bottles. And as those end markets have flagged during the global slump, the price of methanol has crashed. After topping $800 a ton in January 2008, methanol now costs $200. So many methanol producers have been busy closing high-cost facilities and mothballing projects. In short, there’s been a serious industry shake-out. Nonetheless, some low-cost producers are making money even at $200 a ton. These groups are set to dominate a booming market in the coming years, especially as the Chinese come to rely on their output. While China might produce plenty of methanol, local prices are the highest in the world at $240-$250 a ton, notes Mayer. That makes it cheaper for Beijing to import. Giant low-cost producers exporting to China will have a field day as the price of methanol rebounds.

Predicting that rebound isn’t easy. But the signs are good – the methanol price tends to be correlated to rising oil prices and deliveries to Europe and North America have been escalating in recent weeks. With supply being scrimped as high-cost producers shut down, the price of methanol may have bottomed, says Jacob Bout, an analyst at CIBC World Markets. And that presents an opportunity. As Mayer points out, “the time to buy these commodities is when they are beaten down – like now”. We have a look at one prime methanol producer supplying the Chinese market below.

The best bet in the sector

Methanex (Nasdaq: MEOH) is the world’s largest producer of methanol, with 15% of the global market. It owns methanol facilities in Chile, Trinidad and New Zealand. About 40% of the company’s sales are in North America, 30% in Asia and 30% in Europe.

This low-cost producer has the best, and most flexible, plants in the world, says Chris Mayer in Capital & Crisis. Furthermore, it is one of the few producers still generating good cash flow, even with the methanol price down at $200 a ton. It is also protected by a big-industry entry-barrier: the replacement cost for facilities such as those run by Methanex is around $700 per ton.

But the firm has also suffered a number of disruptions to supply in recent years. Its Chilean facility is running at around 60% capacity after Argentina blocked gas exports. But given that the company has largely weaned itself off Argentinian gas, and methanol prices are bottoming, there is strong support for the 6% dividend.

Its overall finances are solid, with $312m in cash against $830m debt. Most of that debt was taken on to complete an Egyptian project, which will generate 1.5 billion tons of the cheapest methanol in the world next year. “On potential production, Methanex trades for only $142 per ton,” according to Mayer. The forward p/e is 12.