As the Dubai property boom implodes, The Sunday Times’s Peter Conradi suggests you invest in the sultanate’s neighbour, Oman. Until recently, foreigners weren’t allowed to invest in property there. Now they can, but only in “integrated tourist complexes”. These developments are “typically built around five-star hotels, marinas and golf courses”, says Conradi, and come with residence visas for the buyer, their immediate family and two domestic servants. So you can embark on a new life in an oil-rich country where the sun shines year round and the ocean is on your doorstep. Add the fact that you’ll pay no capital gains or income tax in Oman and it’s a “tempting prospect”.

Sadly, Oman’s property boom is likely to be little more than a mirage – and one that sounds remarkably like Dubai’s. The developments are huge – the first will consist of 4,000 homes – with tiny properties “pressed closely together on modest plots”. These shoe-box homes don’t come cheap. An 82 sq m one-bedroom flat will set you back £210,000. But at least it’s in a convenient location – right next door to Muscat airport.

Pundits argue that Oman is a better bet than Dubai because it’s pursuing a steadier process of development. Perhaps they haven’t noticed that it’s currently building an entirely new town in the desert northwest of Muscat. The Blue City will have accommodation for 200,000 people when it is completed in 2019. What’s unclear is where these 200,000 people will come from. It’s this rampant overbuilding, combined with the economic slump, that has helped derail Dubai’s boom. The latest property price indices for the country haven’t been released yet, but the Gulf Times reports that prices at Dubai’s leading development, the Palm Jumeirah, have fallen 50% in six months.

Another fear is Oman’s track record. Last October thousands of tourists found their holiday plans cancelled when Oman announced that the Gulf Co-operation Council Summit would take place from 26-30 December. Every room in six of its leading hotels was requisitioned for the conference, causing thousands of bookings to be cancelled. A country that tolerates foreign investment rather than welcoming it isn’t a reassuring prospect for anyone thinking of sinking thousands into off-plan properties. In short, we suspect that if you’re patient, you’ll find better opportunities closer to home long before Oman is ever worth buying into.

A week in the property market

• Rightmove’s latest house price index showed a 0.9% rise in house prices this month. The index, which is based on asking prices, reports that the average house price is now £218,081, down 9% on this time last year.

• Meanwhile, the FT House Price Index reported a monthly drop of 1% in house prices in February, leaving the average house price at £200,947, down 13.3% in the past year.

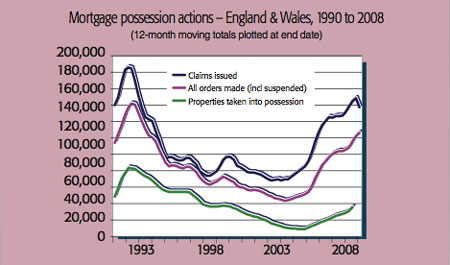

• The number of homes being repossessed in Britain rose by 68% last year, according to the Financial Services Authority (FSA). A total of 46,750 properties were repossessed, up from 27,900 in 2007. The FSA also revealed that the number of people falling behind with their mortgage payments has risen 31% in 12 months. At the end of last year, 377,000 mortgage accounts were in arrears by 1.5% or more of their loan balance – meaning these people are roughly three months behind with their payments (see graph above).

• The FSA also announced that 16.5% of new mortgages granted to single-income applicants, and 20% granted to applicants on joint incomes, in the last quarter of 2008, were self-certified. These mortgages rely on people informing the bank of their income on their mortgage application, without any checks being made. As such, they are frequently referred to as ‘liar loans’, as applicants have been known to exaggerate their income. As a result they have produced the greatest arrears problems for lenders over the past year, and yet “their prevalence has fallen only slightly in the past year and a half since the housing bubble burst,” says the BBC.