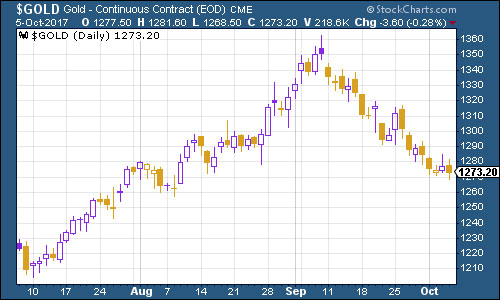

Gold has suffered another steady drift lower this week. North Korea didn’t do anything more to rattle the horses, and the dollar continues to pick up pace. Meanwhile, the S&P 500 is enjoying an epic winning streak and that makes gold look dull by comparison.

(Gold: three months)

The US non-farm payrolls data is usually desperately important to the market. But this month’s is entirely up the spout (that’s the technical term) because of hurricane disruption. So the fact that the US actually shed 33,000 jobs last month had little impact, because no one really knows what the ‘real’ number is.

The US dollar index – a measure of the strength of the dollar against a basket of the currencies of its major trading partners – continued to pull itself higher this week. US economic data has been fairly healthy (while it’s very hard to gauge what’s going on with employment right now, a key survey of manufacturing activity hit its highest level since 2004 – although it’s worth noting that this has been put down partly to the hurricanes as well).

(DXY: three months)

It also didn’t help that sentiment towards the euro soured somewhat given the sticky situation over Catalonia. As the weekend approached we weren’t much closer to any kind of resolution – Spain seems pretty determined to prevent any potential move towards independence.

The Catalan chief of police has been accused of sedition, while Spain’s Constitutional Court suspended a session of the Catalan parliament that had been planned for Monday. Apparently, Catalan president Charles Puigdemont now plans to address the Catalan parliament on Tuesday coming. So it should be another interesting week on that front.

Meanwhile, the yield on ten-year US Treasury bonds has ticked higher again. Again, signs of strength in the US economy – and hope that we might see growth and wages pick up strongly at some point – are the main driver.

(Ten-year US Treasury: three months)

Copper had a strong week, suddenly rallying hard after a tough fortnight or so, partly down to an earthquake in Chile that threatened supply disruption.

(Copper: three months)

It was also another solid week for bitcoin (if you missed my colleague Charlie Morris’s piece on this in MoneyWeek earlier this month, do have a read at it here). Various countries are discussing or rejecting bans on various aspects of the cryptocurrency revolution, but much of this is aimed at ICOs (initial coin offerings) or other more fringe elements of the sector.

This week, weekly US jobless claims continue to be disrupted by hurricane activity but this is starting to ease off now. The four-week average slipped back to 268,50 as claims came in at 260,000, a little lower than the 265,000 expected.

According to David Rosenberg of Gluskin Sheff, when US jobless claims hit a “cyclical trough” (as measured by the four-week moving average), a stock market peak is not far behind (on average 14 weeks), a recession follows about a year later.

So far 20 May has been the cyclical trough, but the stock market has only just set a new peak, and the disruption to the US jobless claims means we can’t get a clear reading. So again, the jury’s still out on this one.

The oil price (as measured by Brent crude, the international/European benchmark) slipped somewhat after its recent strong gains. That’s after a five-week winning streak.

(Brent crude oil: three months)

Perhaps unsurprisingly, now that the price has gone up a fair old way, markets are starting to fret about oversupply again. What’s also interesting is that the big gap between Brent (the price in the chart below) and WTI – the US benchmark, which is a good bit lower – is encouraging US crude exports to rise sharply. (The gap between the two – the spread – expanded after Hurricane Harvey reduced US refining capacity, which in turn meant that crude stockpiles built up).

The US is now exporting nearly two million barrels of oil a day (mostly to Canada), which is frankly astonishing if you consider that in 2003, it barely exported any oil at all.

Finally there’s Amazon. The online retail and publishing giant had a better week as the markets in general rallied hard.

(Amazon: three months)