The FTSE 100 is now in official bear market territory. It has fallen more than 20% below its 2007 peak. And there may well be further to go. Nicola Horlick, chief executive of Bramdean Asset Management, recently warned that the full effects of the credit crunch could take “three years to work through the financial system”. Capital Economics’ Roger Bootle went one better by declaring that “it could be five years before things return to normal”.

However, although “institutional investors are reluctant to invest”, as Grant Thornton’s Philip Secrett notes, private-equity buyers are poised to snap-up cheap shares. And these buyers will be hunting on London’s Alternative Investment Market (Aim), claims consultancy Absolute Strategy Research.

Private equity: down, but not out

Private equity is not flavour of the month. The Independent’s Jeremy Warner accuses Texas Pacific Group of “trashing its reputation” by pulling out of a £180m deal to refinance beleaguered building society Bradford and Bingley. Meanwhile, the FT notes, in an article entitled “Death knell sounded for private-equity boom”, that the value of British buy-outs has plummeted from £24.5bn in the first half of 2007 to just £10.9bn so far this year – resulting in jobs being cut at banks such as Citigroup and Goldman Sachs. Mark Pacitti, a corporate finance partner at Deloitte, sums it up: “I am desperately trying to find some good news but it is hard to find any.”

However, while the spending spree that saw private-equity groups gobble up the likes of Alliance-Boots and Foxtons has been terminated by banks refusing to lend, the head of investment banking at Noble, John Llewellyn Lloyd, claims that “there has been a continuing interest in private-equity backed public to privates” – but at the smaller companies level. And this is “undoubtedly positive for the Aim market”. That’s because, being smaller, perceived as riskier and featured relatively infrequently in research reports means many Aim companies now look very cheap indeed – and can be bought by private-equity firms using very little debt.

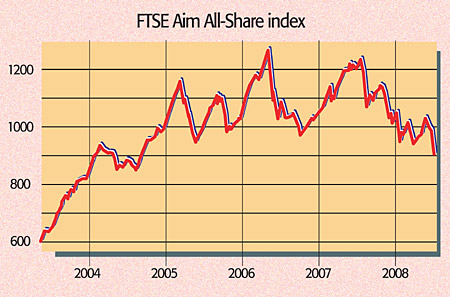

Taking Aim – the risks

The Aim market is home to well over 1,000 small, sometimes fast-growing, companies from a huge range of sectors and countries, which have raised funds at the London Stock Exchange without having to clear the big regulatory hurdles facing firms in the main market. That’s a recipe for some great returns, but also some pretty sizeable risks as Tanfield’s (TAN) recent fall from grace illustrates – the share price of what was until recently Aim’s biggest company sank 83% following a dramatic profit warning.

And the announcement of an investigation by accountants PricewaterhouseCoopers reinforces the dangers of this market, which, according to The Daily Telegraph’s Ben Bland, “is riddled with Tanfields”. He’s right and it is also the case that even perfectly sound Aim firms can still be difficult for ordinary investors to trade, due to wide bid-to-offer spreads that push up trading costs.

Why Aim appeals

Nonetheless, private-equity groups – many of whom “still have a healthy level of funds waiting on the sidelines” – are already on the look-out for targets with “healthy cash balances and strong growth potential”, says Absolute Strategy Research (ASR). This time round, ASR expects to see Aim predators emerge predominantly from economies such as Japan, China, India and the Middle East. Private investors in turn might want to snap-up shares in these firms before big p/e buyers make their move.

Those who did just this in 2002, a couple of years after the dotcom crash, did well – partly thanks to takeovers and partly as “UK mergers and acquisition activity appears to have been something of a leading indicator for the subsequent recovery in share prices”.

The selection criteria

ASR’s “watch list” uses four criteria to pick stocks. First, the target must be something big enough to attract interest yet small enough to be easily digestible without recourse to too much debt financing on the predator’s part. So a market capitalisation of £15m to £100m is a good start. Then, given that cash is king right now, every firm on the list must carry “negative net debt”. Cash balances must therefore exceed short- and long-term interest-bearing balance-sheet debt so it can meet its key cash commitments (such as paying suppliers) even if faced with economic headwinds.

The third main criteria is a decent level of third-party commitment – ASR look for firms that are already backed by an “investment” firm, such as a venture capitalist, with an equity stake of at least 10%. This also needs to be supported by employee involvement so that investors and staff alike are motivated to increase profits – ASR like a minimum total employee equity stake of 5%.

Finally, any firm hoping to become a target must offer a valuation that “does not look excessive”. Here, ASR look for three indicators: a low pe ratio, a low price-to-cash flow ratio and a decent cash flow yield (one year’s “free cash flow” – essentially operating cash flows less non-discretionary costs, such as debt interest and tax – as a percentage of the current share price).

Firms that cut the mustard

Aim investing is not for the faint-hearted and some of the stocks selected by ASR are heavily exposed to sectors we don’t currently favour, such as construction and recruitment. But, as the FT’s private-equity correspondent Martin Arnold notes, some of them – including oil exploration firm Gulf Keystone Petroleum (LSE:GKP) , software developer Financial Objects (LSE:FIO) , digital surveillance software firm BlueStar SecuTech (LSE:BSST) and Character Group (LSE:CCT) – do look like good bets.