Once again, everybody’s talking about “inflections, turns and bottoms”, says Liam Denning in The Wall Street Journal. This year’s renewed plunge in major indices has been followed by a rally that has seen the S&P 500 gain around 13% and the FTSE 100 8%. Fidelity’s Anthony Bolton has called the bottom (again), while Barron’s last week said that US stocks “probably won’t slide much further”. Value investors James Montier of Société Générale and Jeremy Grantham of GMO have become more bullish of late, noting that stocks look cheap – although that’s not the same as saying they’ve reached a nadir.

But this bear market has had more false bottoms than a conjurer’s bag, and this is likely to be another one. Pessimism reached “extreme” levels early last week, says Jack Ablin of Harris Private Bank, a condition that often heralds a rebound. Citigroup generated optimism with a leaked memo saying it turned a profit in the first two months (although this was before write-offs). The G20 finance ministers’ promise to ensure financial stability and Federal Reserve chairman Ben Bernanke saying the US economy could begin to recover next year if the government can get the financial system working also cheered investors.

But the economic fundamentals haven’t changed. Another fall in US industrial production and accelerating unemployment in the eurozone are the latest reminders that there are so far no “glimmers” of economic recovery, says Andrew Lo of the Massachusetts Institute of Technology. Yet global leaders “seem to have taken a concerted decision to look and sound more optimistic”, says David Prosser in The Independent. The recovery, moreover, depends on fixing the banks, and here we need progress on purging toxic assets. This is the “800-pound gorilla that needs to be removed” before confidence and lending can be restored to the system, says Jim Sarni of Payden & Rygel.

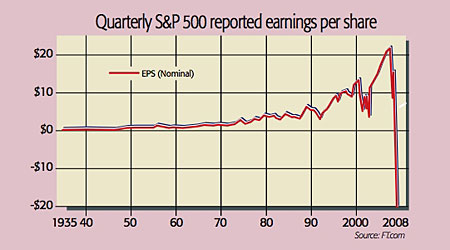

Given this backdrop, “we just can’t see earnings turning up anytime soon”, says Capital Economics; they could be under pressure “well into next year”. With no recovery in profits to look forward to yet, a durable rally will be kept “at bay”. Companies have been haemorrhaging red ink. S&P 500 firms lost an aggregate $180bn in the fourth quarter, due partly to AIG’s record $61bn loss. It’s the first quarterly loss since 1935.

On the subject of American earnings, Investorsinsight.com’s John Mauldin points out that over the past decade or so companies have increasingly emphasised their operating earnings – earnings that ignore one-off charges, such as write-downs – in order to paint a more bullish picture. These “earnings before bad stuff” have come to differ markedly from “as reported” earnings (reported on tax returns). In fact, given expectations of plenty more write-offs, the gulf between the S&P 500’s estimated operating earnings and as-reported earnings for 2009 is 100%. Because operating earnings are widely quoted, they can make stocks seem cheaper than they really are. The S&P’s 2009 p/e based on operating earnings is 11, but based on as-reported earnings it is 22.

To get round this, a good metric is the cyclical p/e ratio, which uses the average earnings over the past ten years, thus smoothing out the profits cycle. In both America and Europe (especially in the former) this measure is not yet at historically rock bottom levels, but has at least fallen far enough to imply “good returns over the ensuing decade”, says John Authers in the FT. But another downleg seems likely, given the ample scope for yet more nasty surprises. The “pain of unwinding the excesses of the credit and mortgage bubble” is far from over, notes Lo, and the global recession is hitting more and more companies. The markets’ “nice bounce”, warns Alan Abelson in Barron’s, will be followed by a “not-so-nice break”.