Pressure Technologies is one of the few exporting success stories left in UK manufacturing, a sector that has suffered decades of decline. This niche firm builds and reconditions the ultra-large, seamless gas cylinders used to stabilise floating off-shore oil rigs in rough seas.

Last year the energy sector accounted for 85% of turnover and just two large foreign platform makers were the source of most of that. Undoubtedly this heavy dependency is the biggest single risk facing the company, which is why the board is actively diversifying into other areas such as aerospace, defence and industrial gases.

For example, the company recently secured a prestigious £3m contract with the French Navy for its next generation of submarines.

This contract helped it to end September with a record £23m order book, to which oil and gas work contributed just two thirds. This suggests a broader revenue mix going forward.

In addition, Pressure Technologies is also trying to establish a foothold in the nascent British bio-gas market, where cylinders are used to store methane for later consumption in hybrid vehicles, or by the national grid. On top of that, the firm is currently being boosted by the lower pound – last year 88% of its £23.7m turnover was derived from overseas territories.

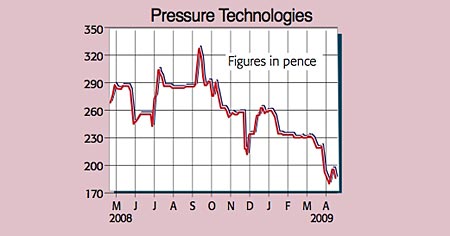

Pressure Technologies (Aim:PRES)

House broker Brewin Dolphin has pencilled in 2009 sales and underlying earnings per share of £25m and 33.5p respectively, rising to £27m and 36p in 2010. The prospective dividend yield is a healthy 3.5%, while the shares trade on rather lowly p/e ratios of 5.5 and 5.1 for the next two years. This is despite the company sporting a cast-iron balance sheet, which includes net funds of £5.9m.

So is there anything to watch out for? Along with a high customer concentration and its foreign exchange risk, Pressure Technologies is exposed to a falling oil price. This could point to less deep-sea drilling and even order cancellations.

The shares are also thinly traded, so if you wish to buy some, I’d advise against chasing up the price. All that said, the risks are more than outweighed by the very low share valuation. With global energy demand set to increase long term, this minnow should be well placed.

Recommendation: Speculative buy at 185p (market capitalisation £21m)

• Paul Hill also writes a weekly share-tipping newsletter, Precision Guided Investments