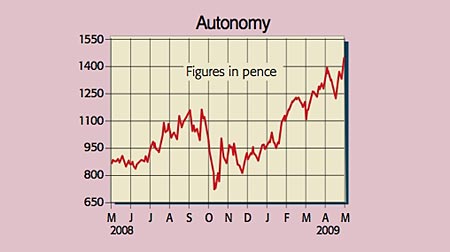

Legendary investor Warren Buffett once cautioned investors to be “fearful when others are greedy”. So I’m fearful for investors in Autonomy, the Cambridge-based software house. Its shares are trading at near all-time highs. The firm is a UK success story, but I would not pay £14.87 for the shares. That’s equivalent to a racy 22 times 2009 EPS (at 65.4p) and seven times sales.

Autonomy’s proprietary technology – ‘e-discovery’ – addresses the complex problem of rapidly searching through vast swathes of unstructured data. Using advanced pattern recognition, the software can trawl through data sources such as spreadsheets, documents, presentations, emails, acrobat files, telephone calls and even video clips.

Customers use it for everything from counter-terrorism and research and development, to complying with statutory requirements. It has come into its own recently as clients have used it to try to protect themselves from litigation arising from the subprime fiasco.

Autonomy (LSE:AU), tipped as a BUY by Panmure Gordon

First-quarter results were cracking. Sales leapt 23% and profit margins shot up from 30% to 45% on the back of strong organic growth, a first-time contribution from its $775m acquisition of Interwoven and an improved cost structure. But although recent growth, and the uniqueness of Autonomy’s products, are impressive, I have doubts about the future. Competition is hotting up and this lucrative sector will be far more cut-throat in two to three years’ time.

Microsoft is beefing up its search credentials with some highly rated products such as Vista and Sharepoint, and Google and Yahoo are likely to start exploiting their immense internet search capabilities soon. And this industry is infamous for one-hit wonders (for example, Netscape) that either failed to keep up with the break-neck pace of change, or were unable to compete against Microsoft’s very deep pockets.

Finally, good though Autonomy’s software is, purse strings within its core customer base are being tightened. I suspect winning new licences is becoming harder. It’s time for investors to get out.

Recommendation: SELL at £14.87

• Paul Hill also writes a weekly share-tipping newsletter, Precision Guided Investments