Our experts at this month’s Roundtable are divided on the question. Here they tell us where they would – and would not – put their own money now.

This month’s panel is made up of: Nick Brind, Fund manager at HIM Capital; Max King, portfolio manager at Investec Asset Management; Tim Price, director of investment at PFP Wealth Management; and Victoria Stewart, senior UK equity fund manager at Royal London Asset Management.

John Stepek: So is this a new bull market, or is it still a bear-market rally?

Tim Price: The situation is confused. You’ve had a big surge in equities and a retrenchment in bonds. The underlying economic reality hasn’t really changed – if anything it’s got worse. So how do you assess value? In the absence of any clear idea, you go with the technicals. And the technicals look increasingly as if the bear market is over. It’s not a high-conviction call, but in the absence of more clarity I have to go with that.

Victoria Stewart: I agree, it’s difficult to hang on absolute valuations given that we don’t really know if we’ve got the trough in earnings yet. But when you look at equities versus property, versus bonds, you can see relative value in equities. Also, if you look at the potential economic outcomes, equities are attractive. If you think policy stimulus is overdone and we’re facing inflation, you’d probably plump for equities. If you think the recovery is on, you’d buy equities too. It’s only if you really believe we are heading back to a depression-type scenario that you wouldn’t buy equities.

I think we’re in the early stages of a pretty long-term bull market, with little short-term downside and lots of long-term upside

Max King: Three months ago, here in this room, I banged the drum for the bull market, and I think we’re in the early stages of a pretty long-term one. I see little short-term downside and lots of long-term upside. The most encouraging thing is that the earnings story is turning round – around the world there are more earnings upgrades than downgrades. It’s certainly not too late to pile in. In fact, it’s dangerous to sit on the sidelines and watch it going up without you. It’s also far too tempting to take profits and wait for a correction – it’s not going to happen.

Tim: Wouldn’t you concede that there’s not enough volume yet to make this a high-conviction call? The market is ‘melting up’ with a lack of real engagement by institutions.

Max: Actually, I’ve been surprised that the market hasn’t gone up more rapidly. I thought we’d see a greater vertical rise on lower volumes. It’s gone up pretty steadily with reasonable volumes. If you think back to when the UK market turned in the mid-1970s, it doubled in three months on virtually zero volume.

Nick Brind: I do think we’ve entered a new bull market, but there are headwinds. The banking system is having daily injections of adrenaline to keep it going, so it’s going to be volatile. The bear argument would be that if you look at the long term, using cyclically adjusted p/es, then equities are cheap, but not as cheap as at the lows of previous big bear markets. But the response has been very different from previous cycles. So I think we’ve seen the lows, but it won’t be all plain sailing.

Max: Actually, it’s only in the 1970s that p/es were lower than at the bottom this time around. But that is a total illusion due to inflation. If you adjust for inflation you find that p/es weren’t nearly as low as they have been recently, because several times in the 1970s, inflation basically destroyed the real profitability of the British market.

John: But how does this all play out? What happens when they pull the plug on quantitative easing [QE]?

Max: I’m still bearish on government bonds. When QE is reversed, government bond yields are going higher. The UK has a big fiscal nightmare ahead of it. But that’s all economic stuff. The UK market is not about investing in the UK economy.

Tim: But the real concern surely has to be that if bond yields are rising already, even during a period of QE, then what on earth will happen when they turn the corner?

Max: I suspect the US administration is already concerned about bond yields feeding through to mortgage rates. So I reckon it will take more prompt action to bring the fiscal deficit under control than in Britain. So the rise in bond yields in the short term is good news, because I think it increases the chance that governments will take it seriously.

John: Any thoughts on how the trouble in eastern Europe could play out? Is it likely to hurt the euro?

There has to be a risk that if the US government has to restructure its debt, we have a currency crisis par excellence

Max: I think so. There are strains on the euro, and the easiest way to relieve those tensions is for the euro to go down against the dollar and maybe even against sterling. My guess is sterling will probably go to €1.25 or €1.30. I hate being positive on sterling against any currency, but…

Tim: But in so many investments right now there are so many things that are the ‘least worst’ option. Sterling feels like the least worst G7 currency.

Max: I agree – although I think sterling against the dollar at $1.60 looks expensive again, so I’d actually be very happy to buy the dollar again at $1.60.

John: Will commodity prices keep rising?

Tim: I think so. My biggest concern in the long run is government indebtedness, particularly in Anglo-Saxon economies. How much has the US government pledged to support the banking system? $11trn? More than the cost of the Marshall Plan, the Vietnam War, the space race – everything put together, with the exception of World War II. The figures beggar comprehension.

There has to be a risk that if the US economy doesn’t eventually revert to something close to its previous levels of growth, the US government will have to restructure its debt. If that happens, we have a currency crisis par excellence. So there’s every reason in the world to start thinking: ‘OK, where are the obvious anti-dollars?’ And the obvious anti-dollars are gold, oil, raw materials, etc.

Max: I agree. Logic says America will knuckle down and sort the problem out, but my money says I’m more than happy with gold.

Nick: Lack of access to capital for discoveries or new investments will have an effect too. Look at the mid-1990s: the oil majors were obsessed with cost and so cut back on exploration. It wasn’t until six or seven years down the line you saw the impact that had.

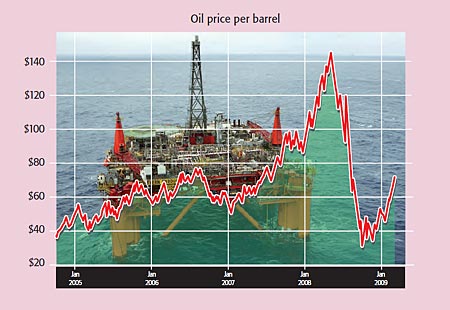

Max: Our view is that a reasonable oil price this year would be around $55 – we see $80 as a three-year target. But all our research shows that in the long term the energy sector is not correlated to the oil price. Extra returns from high oil prices are quickly arbitraged away by costs and governments. So although I’d be a bit cautious on the oil price in the short term, you should stick with the sector as an investment play.

John: Given that ports are full and there are fleets of ships loaded with oil, why is the price so high?

Tim: I completely share your scepticism. I find the idea that the oil price is high due to anything other than ridiculous speculation hard to believe.

Max: It’s possible that the global economy is a lot stronger than the numbers suggest, and that’s why the oil price is high.

John: Let’s talk about emerging markets. Max, you mentioned Russia last time.

Max: Emerging markets are overbought in the short term. People seem to think that by piling into emerging markets you can catch up on the bull markets you’ve so far missed. That said, Russia still looks very good value – I think that’s got further to go. Everyone loves Brazil, but the Brazilian currency is very, very expensive. The Brazilian real is, I think, 220 to the dollar. I reckon you’ll see it at 350 again. US interest rates are 0%-0.5%. In Brazil, they are 9.25%. So to sell the real and buy the dollar is a pretty expensive thing to do. But as Brazilian interest rates come down, the real will come under pressure. So I think there are question marks over Brazil in the medium term.

Tim: But again, taking a slightly longer view, where would you rather invest? Clapped out Anglo-Saxon economies that are basically bankrupt, or a much younger, more economically vibrant and more fiscally sound part of the world? It’s a no-brainer.

John: So what should we be buying now?

There is some very good value in large defensive stocks, and attractive yield too

Tim: For me, the market falls neatly into two types of stocks. The first is the extremely defensive stuff. We are still in a global recession and you want to own businesses that are still going to be around in a few years’ time. The other type are stocks that until recently were completely bombed out, mainly mid-caps or small-caps. These tend to be industrials, mining and commodities groups, and are still on what looks like a very fair rating. They will give you more growth if you can weather the volatility.

Victoria: There is some very good value in large defensive stocks, and attractive yield too. So if your capital growth isn’t great, you’ve at least got the yield pick-up. The stocks that got ahead of themselves are the consumer-oriented ones, which were the first to go down and first to recover. But unemployment is coming through much faster each month, so I think that’s an area for caution.

Max: The areas I picked out three months ago were emerging markets, small caps and gold. I still like those for the long term, but they’ve done well, so I’ll pick another three. Private equity funds are very cheap. You can buy some at scarcely half their asset value – Pantheon (LSE: PIN) is at a more-than 50% discount to asset value; Intermediate Capital (LSE: ICP) is about 40%-45%; and Electra (LSE: ELTA) is about 30%. I think they have a long, long way to go. Those are my high-risk, high-reward picks.

Nick: It’s the mid-market shares where the opportunities lie. They didn’t have the excesses of leverage that the large buyouts had; they’ve got the cash. So two smaller ones are worth looking at too, mid-market specialists. Graphite Enterprise (LSE: GPE) and Dunedin Enterprise (LSE: DNE).

Max: In the middle of the spectrum with regard to risk is Japan. Japan has the most rapidly improving earnings fundamentals and economic fundamentals of anywhere in the world. The consensus forecast for Japanese earnings for this year has gone from –10% to +20% in the space of a couple of months.

Tim: That’s analysts for you!

Max: Two funds I like are the Morant Wright (LSE: MWJ), which is a value small-cap fund, and our internal unit trust, the Investec Japan Fund (tel: 020-7597 1900). Like many others, we’ve closed down the onshore version because of lack of interest – a clear bullish sign. So you have to buy the offshore version. But don’t be put off, it’s very positive that these funds have been closed down. On the more cautious end, I’d go for pharmaceuticals. I think they command both value and growth, but are being left behind. That’s a happy hunting ground. I’d go for the Finsbury Worldwide Pharmaceutical Trust (LSE: FWP) or the Biotech Growth Trust (LSE: BIOG).

Nick: What about some of the hedge funds? Surely the opportunities available now are massive if they can take advantage?

Japan has the most rapidly improving earnings and economic fundamentals of anywhere in the world

Tim: Thames River Hedge Plus (LSE: TRMA) is one of the more aggressive funds of funds. Like everything else, it got whacked last year, but it’s looking pretty healthy at the moment.

Victoria: In the small-cap area some of the good quality, more defensive growth names have come right back in valuation terms – such as veterinary group CVS (LSE: CVSG), or funeral provider Dignity (LSE: DTY). Elsewhere, medical technology still offers stocks with very sound business models. We’re still positive on diagnostics group Axis-Shield (LSE: ASD) and one of the smaller names, ProStrakan (LSE: PSK). It buys in existing compounds, re-engineers them, then sells them in different formulations. It might be a tablet they make into a patch, for example. Their big drug has just gone to market in America.

Nick: One high-risk one is International Personal Finance (LSE: IPF). It’s a door-to-door lender. It emerged from Provident Financial and operates in eastern Europe and Mexico. It’s had a couple of slip ups and there is obviously the risk of volatility in eastern Europe. But door-to-door lending has a very high margin and it’s different from banking – you’re not borrowing short to lend long, you are borrowing long to lend short. Its profits have been depressed by the fact that it’s been growing new markets, such as Romania. It’s cheap on price, cheap on p/e – risky short term, but a great business. And if the current management can’t get it to perform, I’m sure someone else will do the job for them.

Tim: Two personal favourites are engineer Weir Group (LSE: WEIR) and temporary-power provider Aggreko (LSE: AGK). Aggreko is up 30% year to date; Weir is up 80%. Yet they’re both trading on very sub-market multiples, so I would be comfortable holding and buying now.

John: Can anything spoil the party?

Nick: Yes. We have this whole experiment going on: the belief that QE will solve our problems. But only time will tell whether it does, or the economy ends up looking more like that of the 1930s.

Max: You have to come back to the fiscal problem, which is most acute in Britain. I think people are still assuming that somehow it will be solved. But the primary deficit in the UK is going to be 9% of GDP next year. The incoming government will have a huge headache. Economist Tim Congdon reckons that the government will have to raise taxes by 2% of GDP the day it comes into office. That, I think, is about 6p on the standard rate of income tax on day one. After that, he says, they’ll have to cut public spending as a share of GDP by 1% a year for five years. This is a huge challenge. It’s possible the government will fail to meet it and the UK as a sovereign credit will blow up. So I think that’s the big risk.

Victoria: Yes, the public sector is the big looming issue. Despite the recent shenanigans in the cabinet, the stockmarket isn’t too interested yet. But when we start to focus on a date for the election and manifestos and how we’re going to sort out the problem, the market will start to focus on the drag. Quite a lot of domestic-oriented UK firms are big players in the public sector (construction and service firms, for example) and many investors have become complacent about the availability and profitability of public-sector contracts. But how much new business will be around and what margins will they be allowed to make on that?