One of the central planks of President Obama’s $787bn stimulus package is the creation of a ‘smart grid’ – an electricity network that manages power generation, distribution and consumption more effectively.

An initial $11bn has been ear-marked to get the ball rolling, although the total cost is likely to be closer to $75bn. By anyone’s standards that’s a lot of money, even compared with the gigantic $45bn US electrical contracting market.

The money is not only being spent to stave off a recession, but also to reverse decades of underinvestment in infrastructure.

One business set to benefit is Integrated Electrical Services (IESC), America’s second-largest electrical contractor, and one of the few players offering nationwide coverage.

Integrated Electrical Services Inc (Nasdaq: IESC)

It provides a broad range of services, including designing, building and maintaining electrical, data communications and utilities systems for commercial (63% of turnover), industrial (14%) and residential (23%) customers.

Though demand to install new electricity systems in offices, hotels and homes has tapered off in the slump, the group’s $297m order book has started to reflect growing interest from power stations, wind farms and water-treatment centres.

The business is set to generate revenues of around $700m for the year ending September 2009 and to be profitable on an underlying basis, closing with net cash of around £25m (or $1.70 a share). I reckon it should be able to deliver sustainable EBITA margins of at least 4% by 2011. Assuming a ten-times multiple and discounting back at 12%, this gives an intrinsic worth of $17 a share.

What are the potential pitfalls?

Obviously, the firm is sensitive to the economic cycle, as well as being exposed to the usual concerns (such as pricing and cost over-runs) associated with large-scale projects. Plus its controlling shareholder, Tontine, is exploring the disposal of its 58% stake, which could unsettle the shares until a new buyer is found. Finally, for UK investors there are the foreign-exchange issues of investing in US stocks.

But with a well-respected brand, sound balance sheet and a national footprint, this company looks well placed to gain from the roll-out of America’s new $75bn smart grid.

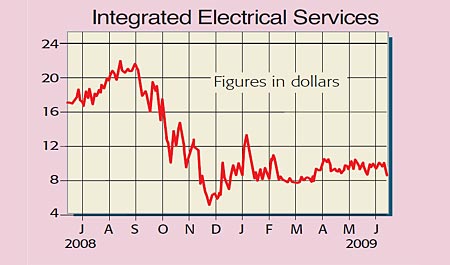

Recommendation: speculative BUY at $8.50 (market capitalisation £146m)

• Paul Hill also writes a weekly share-tipping newsletter, Precision Guided Investments