There’s a popular perception around global warming that it’s not worth bothering doing anything about it because the Chinese are building coal-fired power stations faster than you can say “CO2 emissions”, so we’re all doomed anyway.

But in fact, China has recognised that climate change is a huge restraint on growth and that the country needs to move as rapidly as possible into low-carbon technologies in order to meet its development goals without polluting its own environment even more than it already has. The result is that China has now become a powerhouse for renewables, both as a centre of manufacturing and as a market in itself.

“Some of the fastest-growing companies in alternative energy are based in China,” says Simon Webber, co-manager of Schroder’s Global Climate Change Fund. “As an end market they’ve rapidly switched the mix to alternative forms of energy generation, which has implications for companies globally that play into those industries”.

The Chinese government had previously set a target to build 30GW of wind power capacity by 2020, but this is soon to upgraded, with the new target likely to be between 100GW and 150GW. Meanwhile, solar targets are likely to be raised from 1.8GW to 10GW. New Energy Finance reckons that the green component of China’s ¥4trn (£354bn) economic stimulus package is likely to be £29bn, but that most of this will go towards upgrading power grids and waste and water treatment projects.

On top of this, “China is in the process of drafting another stimulus plan aimed specifically at the renewable energy industry”, says Chi-Chu Tschang from New Energy Finance in Beijing. “There should be more money that will go directly into the solar and wind sectors. But until the stimulus plan comes out, we won’t know exactly how much”.

This means there are huge contracts up for grabs – and Chinese firms, inevitably, will win most of the business. In a recent round of contracts for wind farms, Chinese companies won 74% of the bids. That’s partly because Chinese wind turbines tend to be cheaper than those built by foreign companies and partly down to the ‘70% local content’ rule, which favours Chinese firms over foreign rivals.

A number of Chinese turbine manufacturers will benefit. One larger company accessible to British investors is Hong Kong-listed Dongfang Electrical (HKG: 1072). Dongfang is one of China’s biggest enterprises and is also involved in nuclear power, so it’s not a pure play in renewables, but it’s certainly worth a look for investors looking to buy into alternative energy – China is expanding its nuclear capacity greatly too.

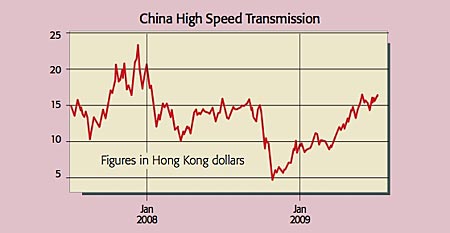

But a better bet for a pure play on the sector is China High Speed Transmission (HKG: 0658), which has a 90% share of the Chinese market for turbine gearboxes. The Nanjing-based company, which also makes marine gearboxes, posted sales growth of 80% to just over ¥3.4bn (£307m) for last year and a net profit of ¥692m (£62m), an increase of 126% over the previous year. It trades on a forward p/e of 21, and yields 1.6%.

There may still be some upside for foreign-owned companies: “local equipment manufacturers are certainly going to get the lions’ share”, says Webber. “But some of the foreign manufacturers will benefit. Vestas and Gamesa both have wind turbine businesses in China that will see some growth”.

Other companies with a Chinese presence include GE, Siemens and Suzlon. The picture in solar power is completely different for the simple reason that (unlike wind turbines) solar panels are easy to transport around the globe. Solar panels have therefore become commodities in a way that wind turbines haven’t: they can be assembled in the cheapest location and shipped anywhere. This has meant that China has become a big exporter of solar panels.

However, the solar industry is currently in the midst of a huge shake-out, as over-capacity in the silicon supply chain has led to a crash in the price of solar panels, and it’s expected that some of the weaker companies might go to the wall.

For this reason Webber urges caution. “It’s very important to pick good quality companies,” he says. “It’s really the first tier of Chinese manufacturers that are going to have the best growth prospects”. He likes companies such as Suntech (NYSE: STP), Yingli Green Energy (US:YGE) and Trina Solar (NYSE: TSL) that are making major inroads into Europe and America, as well as being in a position to benefit from domestic growth.

However, with the softening of solar markets in the West, it’s domestic growth that is likely to drive valuations upwards. Until recently, 95% of China’s solar capacity was exported, but the new targets could change this dramatically. The picture is complicated by the fact that as well as national government targets, provincial governments have also set their own quotas to help develop their manufacturing bases.

Jiangsu Province, for instance, recently announced ¥1bn (£90m) of incentives designed to bring solar capacity up to 260 MW and reach annual polysilicon production capacity of 30,000 tons by 2011. Of all the China-exposed solar stocks, Suntech looks the best bet – it has just announced a 500MW, $1.32bn deal for a new solar plant in Sichuan, on top of a previously announced 500MW project in Qinghai.

The stock now trades at $17 a share, well below its high of $48 last August.

• Nick Hanna is a freelance writer specialising in green investments (

www.thegreeninvestmentguide.com

). He owns shares in Suntech.