America’s recovery is looking “rickety”, said Nomura’s Zach Pandl. Revised figures out this week showed that growth rose at an annualised rate of 2.8% in the third quarter, down from an initial estimate of 3.5%. That’s partly because growth in consumption, which accounts for 70% of the economy, was 0.5% weaker than first thought.

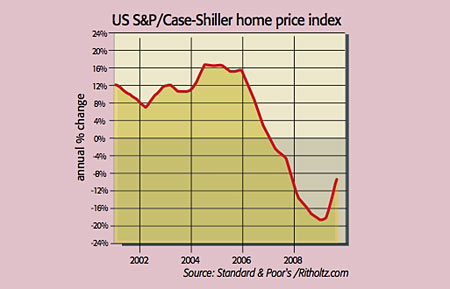

The consumer confidence index rose marginally in November. But at 49.5, it’s still far below the long-term average of 95. The Case-Shiller home price index, covering 20 major cities, improved for a fourth successive month, but the pace of improvement has slowed. Prices are now almost 9% down on a year ago.

What the commentators said

The worry is that as the effects of short-term government stimuli, such as cash-for-clunkers, fade over the next few months, weak underlying demand will keep the recovery “sluggish and fragile”, said Arek Ohanissian of the Centre for Economics and Business Research.

A consumer spending spree remains a distant prospect. Household debt is still at 130% of disposable income, and consumers certainly can’t count on the job market bouncing back any time soon, said David Rosenberg of Gluskin Sheff. History shows that after a credit bust, improvement in the labour market lags positive growth by at least 12 months.

The consumer outlook won’t be improved by the prospect of a renewed slide in the housing market. Housing has also been propped up by “temporary, emergency measures” such as moratoria on foreclosures, and a tax credit for homebuyers, which has just been extended for a few more months, said Saxo Bank. As these dwindle, “expect another leg down”.

At the current pace of sales, there is eight months’ supply in the market, James Hagerty pointed out in The Wall Street Journal – more than the six months of stock that is typically associated with stable prices.

According to one estimate, another seven million homes, or around a year’s worth of supply, could end up on the market in the next few years. Foreclosures are set to rocket due to high unemployment and a jump in mortgage payments, as low initial interest rates on mortgages taken out at the height of the boom reset.

And 12.4% of households with a mortgage are in foreclosure or more than 30 days overdue with their payments, up from 8.6% last year. What’s more, demand is far from solid, said Hagerty. Uncertainty over whether the homebuyer tax credit would be extended wiped 10% off housing starts in October and November. Without government aid, and once the boost from rebuilding inventories fades, growth is likely to “slow sharply” next year, said Capital Economics. As Lex put it, “it’s going to be a long slog”.