Are we in for a period of deflation, or will inflation take off again over the next few years? The ‘conventional’ view on this crucial question for investors is that deflation remains the biggest risk, as Tony Jackson points out in the FT.

That’s because “the world has so much spare capacity”. Put another way, the “output gap” in major economies – the gap between actual and potential GDP – is huge, due to the brutal recession.

The IMF thinks the output gap in advanced economies is 3%-5% of potential GDP. Earlier this year, the Congressional Budget office estimated America’s output gap at around 6% of potential GDP. Such high output gaps imply that there is little prospect of demand exceeding supply in the economy anytime soon.

So inflation isn’t a danger, central banks’ rock-bottom interest rates and money printing notwithstanding. But be warned, says Lex in the FT, “it is almost impossible to measure an output gap with any degree of accuracy”.

GDP data tends to be heavily revised over the years, so policy-makers “will only have a very rough idea” of both the current level of GDP and the levels of GDP over the past few years, says Tim Bond of Barclays Capital.

That makes it very hard to get a handle on GDP, potential GDP and the output gap. Since 1965, the average difference between the output gap calculated in a particular year, and the output gap for that year based on revised data available today, is 1.4%. That’s bigger than the average absolute value of the output gap itself since 1965.

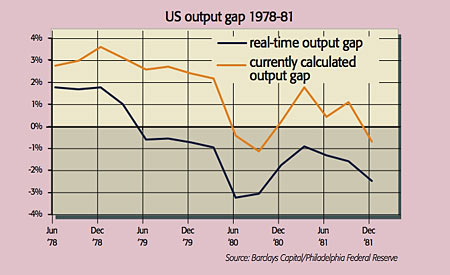

And to confuse matters further, errors in output gap calculations are especially big when the economy is volatile, as it is now. In the 1974-1975 recession, for instance, policy-makers thought that the peak-to-trough fall in GDP was 7.7%. Today’s data suggests it was just 2.5%. And in the late 1970s, the output gap appeared far larger to policymakers at the time (in ‘real’ time) than it appears now based on revised data (see chart).

So “it is easy to see how monetary policy settings” in the 1970s “turned out to be inappropriately loose”. Throw in central banks’ fear of deflation, due to high Western debt levels, and it could well be a similar story this time, says Bond.