One flash point for the general election is the debate over the lack of secure transport for our troops in Afghanistan. First there was the shortage of helicopters. Then, in March, Snatch Land Rovers were blamed for 35 deaths due to their poor record in defending against roadside bombs. Enter Force Protection, a US firm that builds armoured personnel carriers (known as MRAPs) and trucks that clear land mines.

The firm’s top-selling MRAP is the Cougar. It has a distinctive V-shaped hull and a high carriage to deflect explosions, while the sealed cabin is surrounded by the wheel fittings to give added protection and make it easier to repair. More than 3,000 vehicles have been sold so far to a range of customers, including the Canadian, Hungarian, Italian, Polish, American and British militaries. Indeed, so good are these MRAPs that Force Protection has even been praised by the Prince of Wales, who thanked it for saving the lives of hundreds of soldiers. The Ministry of Defence (MoD) is expected to buy another 100-odd units later this year.

Force Protection also sells the Buffalo, the US army’s main weapon for creating safe routes through areas littered with the Taliban’s booby-trap bombs. This truck is the most advanced mine-clearance vehicle in the world. Again, it sports a V-shaped chassis and incorporates a 30ft robotic arm for ordinance removal.

Force Protection (Nasdaq: FRPT), rated a BUY by Merriman Curhan Ford

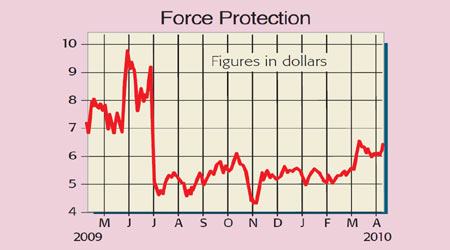

However, supplying the military can be a hazardous business. As you can see from the chart, the shares have been clobbered as competition has intensified, which saw the company lose out to rival company Oshkosh on a $1bn contract for the Pentagon to deliver off-road vehicles in the mountainous terrain of Helmand province. Since then, expenses have been cut to the bone. Resources have been shifted to prioritise more repair and maintenance of in-service vehicles, modernising them with the latest technology, and training soldiers in how to use them properly. Support now represents 70% of revenues, improving both profits and income visibility.

But the firm isn’t abandoning production. Far from it. It has developed a new truck called the Ocelot, which is currently being put through its paces by the MoD, and also being trialed by the Australian army. And following Gordon Brown’s pledge to spend £100m in replacing the Snatch Land Rovers, Force Protection’s board believes that Britain will shortly order 200 of these armoured patrol vehicles.

Wall Street expects 2010 turnover and underling earnings per share (EPS) of $674m and 45 cents respectively, rising to $677m and 54 cents in 2011. The firm also has net cash of $147.3m (equivalent to $2 a share), which leaves plenty spare for strategic product development and simply riding out the ups and downs of the cycle.

Risks include the impact of future army spending cuts, a withdrawal from Afghanistan and foreign-exchange movements. But this is to be expected for defence operators. I’d rate the stock on a four-times gross profit multiple, which, adjusting for the cash pile, generates an intrinsic worth of $9.70 per share.

Recommendation: BUY at $6.47

Recommendation: SELL at £29.20

• Paul Hill also writes a weekly share-tipping newsletter, Precision Guided Investments