Due to the Deepwater Horizon disaster, US law-makers are likely to push through a ream of complex new regulations. So the cost of drilling will skyrocket. This is bad news for the field operators, but means happy days for the large oil services groups who will lap up the required extra spending. Near term, the picture is less rosy, as the White House has placed a six-month moratorium on all deep-water drilling. But given the strategic importance of the Gulf of Mexico to the US economy, this blanket ban will eventually be lifted and drilling will resume.

Enter Technip, the world’s leading subsea supplier of flexible pipe. It’s also a provider of deep-water vessels and a designer of new refineries and petrochemicals plants. Its high-performance flexible pipes, consisting of multiple casings, can withstand pressures of 15,000 pounds per square inch and can handle depths of around 10,000 feet with no risk of rupture. The expertise needed to develop and test them is a big barrier to entry for smaller competitors.

Technip is financially robust. Sales for 2010 should be between €5.9bn and €6.1bn. CEO Thierry Pilenko noted recently that the firm’s clients seem determined to press ahead with projects, such as one in Brazil. Indeed, Technip’s order book closed at a whopping €8.13bn (up from €6.9bn) at the end of March. Net cash held steady at €1.8bn (representing €16 per share). In June the firm bagged a $300m contract in Egypt, a €25m deal in India and a four-year deal with BG in the North Sea.

Technip (EuroNext: TEC), rated a BUY by Nomura

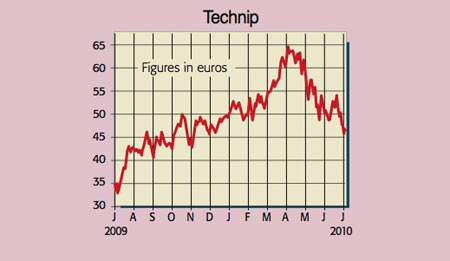

At €48, Technip trades on a bottom-of-the-cycle p/e of 13.6 and offers a 2.7% yield. I would rate the stock on a through-cycle earnings before interest, tax and amortisation (EBITA) multiple of ten. Add the cash pile and I get an intrinsic worth of some €70 per share.

That said, the oil services complex is inherently volatile due to commodity, exploration, production, geological, political and even weather-related risks. And the large turnkey projects undertaken by Technip also carry significant execution risk and scope for final margins to stray off budget.

Even so, the stock is the ultimate pick-and-shovels play on deep-sea drilling, offers 40% upside, and looks a solid buy despite the embargo in the Gulf of Mexico. This is especially the case given that one of its main rivals, Haliburton (which was one of BP’s contractors on the Deepwater Horizon spill), is being sucked into a quagmire of lawsuits and compensation. Results are due out on 22 July and Nomura has a price target of €75per share.

Recommendation: BUY at €48