Brutal price wars are hitting European supermarket shelves. That’s great news for thrifty shoppers, but a nightmare for firms such as Procter & Gamble, the world’s largest fast-moving consumer goods (FMCG) firm, owning 22 billion-dollar-plus brands. These include household names such as Pampers, Ariel, Pringles, Pantene, Bounty, Olay and Gillette. Thanks to its diverse portfolio of businesses, wide geographical footprint and leading franchises, Procter & Gamble is considered to be a safe bet. It’s recently been increasing volumes, expanding margins, and beefing up support for its brands. But I see danger ahead.

Prices are heading south in many of its biggest markets and raw material costs are rising to squeeze profits. The company’s juicy 20.7% Ebita margins look very vulnerable, especially as Procter & Gamble is having to ramp up advertising to differentiate its products. Worse, supermarkets such as Wal-Mart, Tesco and Aldi are demanding bigger discounts, introducing their own cheaper varieties, and even delisting products en masse. With thousands more own-label products being introduced, branded goods will inevitably lose shelf space.

Also, cash-strapped consumers are cutting back in North America. As a rule of thumb, brands can usually only sustain a price premium of up 15% compared to own-label equivalents. With just about every supermarket going hammer and tongs at each other, prices and margins on branded products are set to decline. Lastly, more than half of Procter & Gamble’s top-line growth is attributed to emerging markets, some of which are grappling with serious sovereign debt issues.

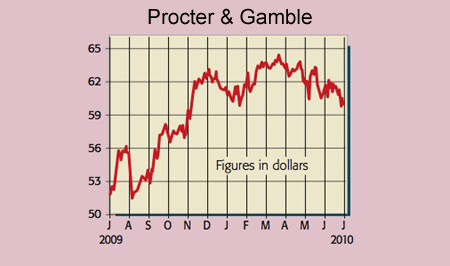

Procter & Gamble (NYSE: PG), rated a BUY by Jefferies

For 2010, the stock trades on rich enterprise value (EV) to sales and EV/Ebita multiples of 2.6 and 12.6 respectively. But I rate the group on a ten-times Ebita multiple – assuming ‘through-cycle’ margins of 17%. After deducting the $25bn debt load, that gives a fair value of roughly $36 per share. The firm may be a quality business with excellent brands, but it is now being dragged into a series of crippling dog-fights to retain market share, while also being hampered by a stronger dollar. Quarterly results are due out at the end of July. Shareholders should get out now.

Recommendation: SELL at $60

Paul Hill also writes a weekly share-tipping newsletter, Precision Guided Investments. See

www.moneyweek.com/pgi.aspx

or phone 020-7633 3634.