Has the British property market lost its marbles again? House prices have bounced 8.3% from the trough in April 2009 (according to Halifax). However, this rally has largely been down to record low interest rates, a dearth of sellers, and a pick up in activity from wealthy overseas buyers taking advantage of sterling’s decline. So don’t be fooled.

It is only a matter of time before borrowing costs rise to choke off inflation, triggered by shop prices heading north on everyday items imported from abroad. For instance, John Bason, finance director of Primark, recently warned that the cost of clothing would climb 5% over the next year as a result of rising Chinese wages. And “this will be more than just a temporary blip”.

Deflationists insist there is still plenty of spare factory capacity, which will keep a lid on inflation. But I think that this time round the CPI will stay elevated. Britain just doesn’t have the same manufacturing base as, say, the Japan, and therefore a lot of what we buy has to be sourced from overseas. So in spite of the Bank of England adopting a loose monetary stance, Britain is on course for a dose of mild ‘stagflation’ – rising inflation and falling growth.

So what does a backdrop of thrifty families with lower disposable incomes mean for Savills, the upmarket estate agent? In short, its British business, which accounts for 51% of turnover, is going to get crushed as transaction volumes dry up and premium property values tumble.

Savills (LSE: SVS), rated a BUY by Oriel Securities

True, there will be a steady stream of foreigners bargain-hunting in Savills’ South East backyard. But this will not be enough to prop the firm up. Just look at what happened between 1973 and 1980 when house prices dived 44% in real terms during a period of stagflation. Lucian Cook, director of real estate at Savills, conceded recently that 6% would be wiped off house values by the end of 2010.

Worse, Savills’ lucrative Asian business (38% of sales) – which was roaring in March – is almost certain to have cooled in quarter two, owing to the Beijing authorities clamping down on mortgage availability. Indeed, last week Chinese banks were warned to prepare for price declines of up to 50% in the major cities. Separately, Savills European outfit (11% of sales) may get hammered, as austerity measures kick in across the continent.

The City is predicting 2010 sales and adjusted EPS of £583m and 15.9p respectively, lifting to £603m and 20.0p in 2011. That puts the stock on lofty price to earnings (p/e) ratios of 19.8 and 15.8. I would rate the group on a through cycle EBITA multiple of ten, assuming sustainable margins of 5%. After adding back the £66m of net cash and deducting the £27m pension deficit, this generates an intrinsic worth of 250p per share.

All in all, with the added worry of higher unemployment and more families opting to rent, it’s time for investors to seek out another home for their cash.

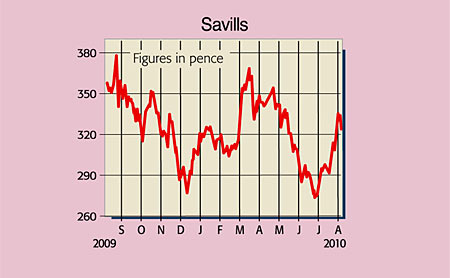

Recommendation: SELL at 315p