The hotel behemoth is a good business, but it’s pricey and overreliant on China, says Phil Oakley.

Fund manager Daniele Gianera made his case for buying InterContinental Hotels’ shares. But while I understand his arguments, I’m inclined to take a more cautious view at the moment.

I agree that InterContinental Hotels (ICH) is a good business – much better than it was ten years ago. The management has worked out that owning lots of hotels across the world may sound glamorous, but actually doesn’t work out that well for investors. Hotels cost a fortune to run and have lots of overheads. They can therefore eat up cash and often produce very poor returns on the money that has been invested in them.

A better strategy is to sell the big trophy hotels, give investors some of their cash back, and franchise brands such as Holiday Inn, Crowne Plaza and InterContinental. This means somebody else takes on board all the running costs in return for a management fee. The improvement in returns at ICH since it followed this path has been startling.

In 2003, the hotels were mostly owned outright and generated operating margins (the amount of revenue that is turned into profit) of 13.5%. Last year – when most of the hotels were franchised – that figure was 33.5%.

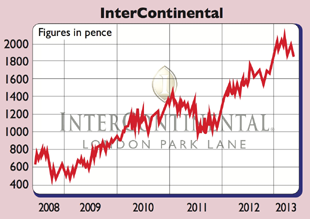

A recovering economy and a growing number of franchisees has seen ICH’s profits and share price soar during the last five years. Bulls argue that the good times can keep on rolling, despite the uncertain outlook for the world economy. The main argument they rely on is the scope for growth in emerging markets, as well as a resilient American business (currently two thirds of profits). At the moment ICH has 4,608 hotels on its books and nearly 700,000 hotel rooms. It has a pipeline of 1,053 hotels and 176,000 rooms, with half of them in emerging markets, with a lot of hopes being pinned on markets such as China.

However, this is where I start to get nervous. On the face of it, growing demand for Chinese tourism and a growing economy makes for a good place to build hotels. My concern, though, is that hotel operators looking for growth outside declining markets such as Europe build too many of them and depress profits for everyone.

The other problem is the price of ICH shares. They currently trade at 18 times 2013 forecast earnings, which is quite punchy considering that earnings are expected to grow by less than 10% this year and next. To me it looks like ICH has joined the list of overly expensive quality blue-chip shares out there.

Buying the shares at current levels therefore looks risky, especially if the Chinese economy weakens. That’s why to me this doesn’t look like the time to buy. Indeed, if you’ve enjoyed the share price rise over the last few years, it might be time to check out and sell.

Verdict: sell

InterContinental Hotels (LSE: IHG)

Share price: 1788p

Market cap: £4.8bn

Net assets (Dec 2012): $317m

Net debt (Dec 2012): $1.07bn

P/e (current year estimate): 18.0 times

Yield (prospective): 2.5%

Interest cover: 10.8 times

What the analysts say

Buy: 12

Hold: 14

Sell: 2

Target Price: 2060p

Directors’ shareholdings

R Solomons (CEO): 728,541

T Singer (FD): 20,846

P Cescau (chair): 0