Where else can you find income like this? Fill your coffers with these shares, says Phil Oakley.

The shares of SSE have proved to be among the most reliable on the British stock market over the last decade or so. Under the leadership of the soon to be departing Ian Marchant, the company has followed a very simple but effective strategy – to increase the annual dividend by more than inflation.

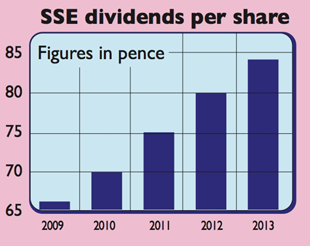

Since Scottish Hydro and Southern Electric got together to form SSE nearly 15 years ago, annual dividends have more than trebled from 25.7 pence per share in 1999 to 84.2 pence in 2013 – an average annual rate of growth of 8.8%. The total shareholder return (the combined return from dividends received and changes in the share price) has been a very decent 360% – much better than the British stock market as a whole. SSE has benefited from having a balanced portfolio of stable, regulated businesses and market-based ones that have given it an attractive combination of stability and growth.

That said, I wonder whether retiring CEO Ian Marchant, 51, thinks SSE’s best days are behind it.

A record of growing dividends

I’ve been overly cautious on SSE shares. Back at the beginning of 2012 I thought they were a sell at 1,212p as I was worried about how much money it could make from selling electricity when power prices were falling, and that big bets on wind farms would not pay off. My concern was that this would hinder SSE’s ability to keep on growing its dividends. But while profits from power generation have fallen quite sharply, SSE’s chunky dividend is still growing and remains highly valued by investors.

Looking forward, making more money from generating and selling electricity is going to be hard. SSE’s retail energy business, which has 9.5 million customers, is busy trying to rebuild its reputation after being found guilty of mis-selling its products. Winning new customers looks unlikely in the short term. On top of that, Ofgem, the industry regulator, wants to break the stranglehold the big energy suppliers have on the market by forcing them to sell more of the electricity they generate to independent retailers.

Meanwhile, low power prices and the rising cost of gas has made generating electricity from gas unprofitable for SSE and others. The government’s decision to have a minimum price for carbon dioxide will make it harder for SSE to make money from its coal stations too. Lots of coal power stations will have to close in the next two to three years.

But there is a potential silver lining here. Britain is running short of electricity capacity and some industry insiders are warning that there is a danger of the lights going out in 2015/2016. This means that SSE’s remaining hydroelectric and wind generating assets could make more money. SSE’s gas stations should also become more profitable. The real grounds for optimism on SSE’s prospects come from its regulated gas and electricity network businesses, which account for roughly half of its total profits.

The electricity transmission grid in the north of Scotland needs lots of money spending on it to connect offshore wind farms and give better electricity supplies to many outer islands. The gas distribution networks in Scotland and the south of England also needs upgrading. This should see SSE’s regulated asset bases grow quite nicely. These businesses should be able to make enough money for SSE to keep growing its dividends for the next few years. Both businesses have just begun an eight-year pricing period, so the risk of regulatory interference, which often worries investors, is quite low.

Elsewhere, there’s much to like about SSE. Despite being a regulated and asset-intensive business, it has a return on capital employed of 13% (better than Tesco and Sainsbury’s). Its finances are in good shape, its debt load is manageable and it has one of the strongest balance sheets of all European utilities. It thus has no problem paying its interest bills.

At 1,525p, the shares offer a prospective dividend yield of 5.8%, which is covered 1.3 times by expected earnings. I think the dividend can keep on growing. With reliable sources of income in short supply, buying shares in SSE and using a growing dividend to buy more looks sensible.

Verdict: buy

SSE (LSE: SSE)

Share price: 1,525p

Market cap: £14.7bn

Net assets (Mar 2013): £5.5bn

Net debt (Mar 2013): £5.5bn

P/e (current year estimate): 13.1 times

Yield (prospective): 5.8%

Interest cover: 4.5 times

What the analysts say

Buy: 8

Hold: 5

Sell: 7

Target price: 1,510p

Directors’ shareholdings

I Marchant (CEO): 222,532

A Phillips-Davies (deputy CEO): 133,816

G Alexander (finance director): 123,732

[xyz_lbx_custom_shortcode id=6]