Everyone wants to buy cheap stocks. But the market usually gets it right. You might think you’ve found a cheap stock, but you then find there’s a terrible business behind it and it turns out that ‘cheap’ wasn’t cheap enough. Yet, sometimes bad firms make good investments. Because they’re unloved, they trade on low valuations. That means they can deliver high returns if things don’t turn out as badly as the market fears.

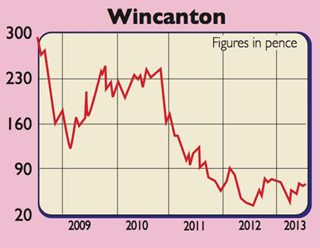

I’m wondering if Wincanton (LSE:WIN) , a British logistics firm, is one of these stocks. At 66p it trades on a forward price/earnings multiple of 4.3 times. That’s low, no doubt about it. But is it too low?

The latest annual report reveals some of the problems. Getting goods from A to B is cut-throat. Two-thirds of Wincanton’s contract logistics business comes from the retail and consumer goods sectors, which are struggling in a weak economy. This can mean less stuff being transported, so less money for Wincanton. Other customers want to save money and are negotiating on price.

What’s worrying is the state of its finances. It had net borrowings (debt less cash) of £107m at the year end. But borrowings over the year are probably twice this. Then it has a near-£150m pension deficit. Throw in onerous lease charges for unused buildings and there’s a lot of cash going out the door. Yet underneath is a reasonable business. It’s winning new contracts and taking out costs, which is boosting margins. It’s offering better services, such as IT and systems support, allowing it to make more money. Profits are set to grow by 9% in 2014/15. Management aims to generate cash and debt should fall.

So what could make the shares a buy? Rising bond yields could cut the pension deficit. An interest-rate swap would protect part of the interest bill, but each 0.1% change in bond yields changes the pension liability by £16m. Falling bond yields have seen liabilities rise by more than the value of assets. Rising bond yields could see this process reverse. With the deficit almost twice its equity valuation, improvements could boost the share price.

Verdict: cheap enough for a gamble