Phil Oakley re-examines two of his share tips from last year to see how they have got on.

Fenner (LSE: FENR)

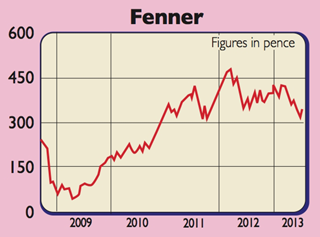

I recommended buying shares in Fenner in February last year. They have not done well and stand 24% below the 455p I tipped them at. Hindsight is a wonderful thing, but it’s obvious now that the risks and the share price were too high back then.

Despite having some good businesses, Fenner’s profits are still heavily influenced by what’s going on in the global mining industry. It is the world leader in supplying heavy duty conveyor belts to mining firms and has been hit by soft trading in its key Australian and American markets.

Moreover, a slowdown in the Chinese economy last year saw less demand for Australian coal and iron ore. The US shale-gas boom weakened demand for coal there. It’s no surprise that Fenner’s customers bought fewer belts and profits fell heavily.

But there is now light at the end of the tunnel. US gas prices are going up and there are signs of some revival in the coal market. Coal stocks are now very low and prices are rising again. China’s commitment to keep its economy growing and spend money on building more railways should help demand for iron ore and coal in Australia, which, in turn, should help Fenner.

I continue to like Fenner’s Advanced Engineered Products (AEP) business. It specialises in niche, problem solving products that are crucial to their customers in areas such as oil exploration, energy, medical devices, diesel engines and package handling. Here profits are more resilient as there is less competition and good growth prospects.

With a recovering mining sector, high oil prices and good prospects for AEP, Fenner’s profits should start to grow again next year. On that assumption, the shares look cheap trading on 10.7 times August 2014 earnings, while offering a 3.5% yield with a growing dividend.

Verdict: buy

Telecom Plus (LSE: TEP)

My recommendation on Telecom Plus has worked out better than my Fenner tip. The shares are up 87% since I tipped them in June last year. The company trades under the Utility Warehouse brand and continues to have an attractive business model.

Its customer proposition is well suited to many cash-strapped households. It sells gas, electricity, home phone, mobile phone and broadband services. The more services a customer buys, the bigger the monthly discount they receive. On top of this, they can use a pre-paid cashback card, which pays rates of between 3%-7% when used at places such as Sainsbury’s and Boots. The money made on the card is then used to reduce the customer’s single monthly utility bill.

Things get better still if the customer becomes a company distributor. This allows them to be paid commission for every new customer they sign up. The rewards can be big. If they become a distributor and one of their customers then becomes a distributor, they get some of their commission as well. It’s not really surprising that there’s a growing number of people making a good living out of this. It’s also great for Telecom Plus, as it allows them to win customers cheaply and boost their profits.

Telecom Plus is still doing very well. Customer numbers are growing at 20% per year, while existing customers are buying more products. Profits are expected to grow by 15%-20% over the next couple of years. But the shares now look too expensive. When I tipped them at 707p, they were trading on just under 20 times earnings but offered a nice yield of 4.2%, as a large chunk of the profits gets paid out every year. Now they trade on nearly 30 times earnings with a yield of 2.7%. As good a business as Telecom Plus is, it’s time to take profits.

Verdict: take profits