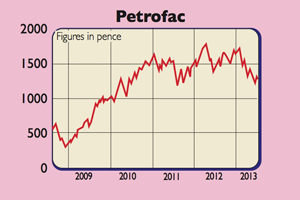

The stock market can be a fickle place. Companies’ shares can be loved one minute and hated the next. It’s not hard to see oil services company Petrofac (LSE: PFC) as one of these cases. The shares, which were trading as high as 1,752p in January, have since fallen by over a quarter.

Petrofac specialises in building infrastructure for the oil and gas sector. Once it has finished building, it often takes over the managing and maintenance of facilities. It also trains oilfield workers.

This has been a nice business to be in over the last few years. High oil prices have seen oil companies spend lots of money looking for the black stuff and getting it out of the ground. Companies such as Petrofac have had lots of work, which has led to a boom in sales and profits. With a big and growing order book, the company became popular with investors and the share price soared.

But times have changed. Earlier this year a terrorist attack on a $1.2bn project in Algeria saw Petrofac evacuate its workers, causing work to stop and – for now – halting profits from the project. Then there has been a series of profit warnings from some of Petrofac’s competitors. Talk of cost overruns, tighter margins, lower orders and losses has caused something of a panic in the sector.

Panic often spells opportunity for investors. I’ve had my eyes on Petrofac shares for a while, but have always thought the market was in love with them too much. At the current lower price, I think the shares are worth a look now.

A lot of the fundamental attractions behind Petrofac’s business are still intact. For one, oil companies are still expected to keep spending money. This is evidenced by the fact that Petrofac is still winning new orders and has an outstanding order book of $11.9bn – almost twice last year’s sales. Petrofac also says it has tight control of project costs and should not experience the same problems as some of its peers.

Although profits are only expected to grow modestly this year – with City analysts expecting earnings per share (EPS) of around $1.90 – the company says that it is still on track to double net profits between 2010 and 2015. This implies 30% profit growth over the next two years and EPS of over $2.50 in 2015.

With a lot of work coming from places such as the Middle East, Africa and former Soviet states, these shares are not without risks, but are cheap if the profit targets can be met. Trading on a price/earnings ratio of 10.2 in 2013, falling to 7.7 times in 2015, the shares look worth a gamble.

Verdict: buy at 1,259p