Five years ago, Johnson Service Group (LSE: JSG) almost went bust. Its dry-cleaning business suffered during the recession as consumers had their suits and dresses cleaned less often. What’s more, the high street’s demise as a shopping destination hasn’t helped matters either. This made it hard for the company to pay the interest bills on its debt.

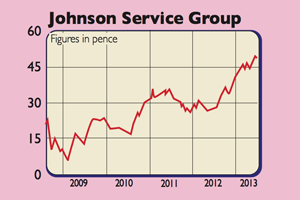

Turnaround specialist John Talbot was brought in to sort things out. He has done a very good job. Investors have put up more money and over 100 unprofitable dry-cleaning shops have been closed. Last week, the company sold its facilities-management business and its portfolio of private finance initiative (PFI) contracts. Most of the debt has gone and the shares have become more popular, with the share price up more than 70% on this time last year. But I think there’s more to come.

Johnson Service makes most of its money from renting out workplace clothing (known as textile rental) and providing dust mats, industrial wipes and washroom hand towels. Trading under Johnsons Apparelmaster, it has 44,000 customers and provides clothing to over a million industrial and food-production workers every week. It also rents out premium linen to hotels, catering and hospitality companies.

This business has been doing well. It is the British market leader, with decent growth prospects. It makes sense for labour-intensive production firms to rent rather than buy workwear. It saves money and hassle: Johnson takes care of the buying, cleaning and delivery of those garments. Its reputation for good service is helping it win new business.

The facilities management business went for less than net asset value, but frees up firepower to expand the workwear unit in Britain and abroad. If the British economy is recovering, it could do well. Dry cleaning is looking up too. It can be hard to make money in this business – margins are wafer thin. But underlying sales are rising off the back of environmentally friendly cleaning services.

Selling the profitable PFI business for a low price will dent profit forecasts, but analysts still expect underlying profits growth of 8%. The 2.5% yield is not stellar, but the firm pays out only a quarter of its profits to shareholders so this has scope to increase.

Trading on just over ten times 2013 forecast profits with reasonable growth, the shares still look good value. It would also not surprise me if its workwear business caught the eye of some support services firms looking to expand their range of services.